by Moe Bedard | Apr 12, 2022 | Mortgage Help |

Homeowners with mortgages backed by Fannie Mae or Freddie Mac are eligible for a two-month extension to avoid foreclosure if they apply to the Homeowner Assistance Fund, according to an announcement on April 6, 2022, by the Federal Housing Finance Agency.

Mortgage servicers will have to suspend foreclosure activities for up to 60 days for eligible homeowners. Assistance can also come in the form of lower mortgage payments and paying utility bills.

“FHFA is committed to sustainable homeownership. Today’s action will provide borrowers who need temporary mortgage assistance with additional time to be evaluated for relief through their state’s approved Homeownership Assistance Fund,” said FHFA Acting Director Sandra L. Thompson.

As of December 31st, there were 178,019 mortgages in forbearance, down from 320,009 in the third quarter, according to an FHFA spokesman, Adam Russel.

Out of the leading states with these mortgages in forbearance, California and Texas ranked number one and three with more than 20,000 and nearly 17,000 mortgages, respectively.

The Homeowner Assistance Fund was created by the CARES Act and is administered by the Treasury Department, provides up to $10 billion to help struggling American homeowners.

Who qualifies for the Homeowner Assistance Fund extension?

To qualify for this two-month extension, homeowners must apply for assistance from the Homeowner Assistance Fund (HAF). The fund covers homeowners who are behind on their mortgage payments due to COVID-19 and don’t have an alternative source of assistance.

Eligible applicants must meet these criteria:

* The homeowner either had a financial hardship caused directly by COVID-19, or they have experienced financial difficulty due to COVID-19 that makes it hard to pay their mortgage.

* They must have a mortgage backed by Fannie Mae or Freddie Mac. To find out if that’s you, go to Fannie Mae’s Lookup Tool or Freddie Mac’s Loan Lookup Tool. Or contact your mortgage servicer directly.

* The original loan must have been sold to Fannie Mae or Freddie Mac before June 1, 2021. Although the loans can be delinquent, they cannot be in foreclosure at least 90 days before applying for HAFA.

* Not already be behind on payments at the time of application.

* Be part of a household with income 80% below the area median income in the location of their property, but only if that amount is no more than $100,000 annually.

* Not have an interest in another residential property at the time they apply for assistance.

The foreclosure moratorium expired on July 31, 2021. However, some states and local governments have temporarily stopped foreclosures.

Homeowners who need mortgage help can visit consumerfinance.gov/housing for up-to-date information on their relief options, protections, and key deadlines.

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Apr 9, 2022 | Mortgage Help |

If you want to buy a home, but don’t have enough money for the down payment or if you are having credit problems, then there is another option.

It’s called the lease option or lease-purchase plan to buy a home.

It’s also a way for those homeowners who want to sell their house, but can’t get their price and those who can’t qualify for a mortgage to come together and agree on a mutually beneficial arrangement.

In most cases, the owner agrees to sell his property for a specific price within a certain time frame and the tenant agrees to rent with an option to buy.

These agreements often require the tenant to pay an agreed upon amount each month toward his future down payment or closing costs, or both.

Not all lease options are created equal.

Some are more similar to rental agreements and offer very little opportunity for the renter to build any equity in the home.

The best lease options give the renter/buyer an opportunity to treat the home as if it was their own, build some equity, and still have time to shop around for financing before taking on the contractual obligations of a mortgage.

This will alllow for a portion of the rent that would be applied toward the purchase if the option is exercised. This is referred to as rent credit.

How it works

You enter into a contract with the seller for a specified time (usually about one to three years), during which you pay rent, and a portion of your monthly payment goes towards the purchase price of the home at an agreed-upon price.

This option means that you can decide whether or not to buy the home at the end, but if you do want to buy it, you’ll have first rights, as long as your contract isn’t up.

The seller keeps all of your monthly payments, minus any rent credits, until you decide to exercise your option. If you don’t buy, he gets to keep all of those payments. You don’t get any money back or credit toward rent.

The option fee is usually nonrefundable and acts as the buyer’s deposit. It may be credited toward closing costs if and when the tenant exercises his or her option to buy.

For example, if you paid $2,000 for an option fee and $5,000 toward closing costs when you bought the house, you’d have $7,000 in equity right off the bat.

In addition to paying rent each month, the tenant pays an extra amount to go toward a down payment on the home.

The more of these “option payments” that get applied to the down payment, the less money will be required from the tenant at closing.

If you exercise your option and purchase your home, your landlord/seller credits your monthly option payments against your down payment.

The lease portion of the agreement outlines the rights and responsibilities of both parties during the lease term, including how repairs will be handled, who pays for maintenance, whether pets are allowed and whether the property can be subleased.

The primary benefit of a lease purchase agreement is that it can allow people with bad credit or no cash to live in a property they might otherwise be unable to buy.

In addition, many sellers of properties under lease purchase agreements are willing to make improvements or repairs to the home before selling it to the tenant.

This gives both parties an incentive to close on the sale: The owners get their money, and the tenants get their repairs.

This type of agreement can be ideal for people who might not otherwise qualify for a mortgage, or who want more time to prepare for homeownership.

Because your monthly payments will generally be higher with a lease-option than with a straight rental, you should carefully consider whether you can realistically afford this type of agreement before signing on the dotted line.

The time frame for when your option expires; if you are not able to exercise your option during this time, you may lose any money that you have paid toward the purchase price.

If you’re thinking about entering into a lease option, make sure you understand what your rights and obligations will be during that agreement period.

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Apr 5, 2022 | Mortgage Help |

The Department of Housing and Urban Development (HUD) and the Federal Housing Administration (FHA) are seeking to initiate a new 40-year loan modification program to help mortgage borrowers and lenders streamline the loss mitigation process.

The proposed rule, published by HUD late last week, would change repayment provisions for FHA borrowers, allowing lenders to modify a borrower’s total unpaid loan for an additional 120 months.

HUD said that this option could prevent “several thousand borrowers a year from foreclosure.”

According to HUD, the proposed change would allow FHA lenders to modify mortgages where borrowers experience long-term COVID-19 forbearance due to job or income loss, or where the borrower is subject to an extension of forbearance or additional payment period.

“This will give these borrowers longer periods of time to recover financially before their mortgage payments go back up to their original amount,” said HUD Secretary Marcia L. Fudge.

As part of the plan, if a lender chooses to offer a 40-year modified mortgage to an eligible FHA borrower, the agency will reimburse 100% of the unpaid principal balance owed on the loan at the time of modification. The reimbursement will be made in one lump sum payment upon completion of all terms and conditions in the modification agreement.

HUD also specifies that the monthly payment on a 40-year loan must be no less than the payment on a 30-year loan because it would not want to encourage borrowers to take out loans they can’t afford.

To qualify for the option, FHA borrowers will need to provide documentation demonstrating functionality in their repayment plans and show that they can afford monthly payments based on their current income levels.

Borrowers must also be current on their mortgage payments for at least 12 consecutive months following the modification under this proposal. The proposal is not available for borrowers who are currently in bankruptcy proceedings or who have already had one or more delinquencies within 24 months of their modification request.

In addition, the proposed rule would allow lenders to process loan modifications for delinquent borrowers in cases where they would otherwise be ineligible due to delinquency. Additionally, HUD said that it is considering additional special application and income verification procedures.

“Since March, HUD has been focused on protecting our nation’s homeowners from the financial impacts of COVID-19 through our innovative loss mitigation strategies and programs,” said HUD Secretary Ben Carson. “We believe that this proposed expansion will allow thousands more struggling families to keep their homes and provide them with time to get back on their feet after this challenging time.”

In June, the FHA introduced a new long-term loss mitigation program for borrowers impacted by the COVID-19 pandemic. The new “waterfall” included a six-month forbearance option, the extension of temporary COVID-19 loss mitigation options, and a new permanent FHA COVID-19 loss mitigation option.

HUD said it believes that this proposed change will help streamline loss mitigation efforts for FHA-insured single family mortgages and will ease the operational burden on its lenders. This new option would allow eligible mortgages currently in forbearance or in default due to COVID-19 related hardships to access longer-term modifications.

The FHA is looking to the mortgage industry to help the agency determine if the 40-year loan modification program is a good idea. The agency is currently taking comments from lenders and other interested parties about the current loss mitigation options, including whether or not a 40-year loan mod should be made available.

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Apr 1, 2022 | Mortgage Help |

Figuring out how much mortgage you can afford is a process that involves several steps. Once you have gone through all of them and have thoroughly examined your financial situation, you can have a much better idea as to how big of a loan you can afford, and in turn, how big of a house to look for.

The general rule of thumb is that about a third of a borrower’s income should be dedicated to financing a home. For example, if someone makes an annual salary of $50,000 a year, they should be able to manage a mortgage of $150,000 if their current debt is moderate.

While this tends to be a common rule for some, it will not be the case for every new home buyer.

A good rule of thumb is to examine your current debt, living expenses, and then adjust for future financial obligations, like children, education, and possible retirement.

Instead of trying to spend all your earnings on buying a home, a more modest approach is sometimes necessary. There’s no better way to be well-prepared for homeownership than making a budget and sticking to it!

Aside from considering your regular monthly costs such as utility bills, car insurance, health insurance, etc. – finding out the exact mortgage costs you will be facing will help you determine whether or not the purchase is a sound financial investment.

You also need to keep in mind that a mortgage loan pays not just for your house, but also for the costs of owning a home, such as insurance, property taxes, and home maintenance. All of these things should be factored into your calculations when you are calculating your mortgage.

There are also many more factors such as your interest rate, credit score, debt-to-income ratios and down payment that affect the amount you can afford to borrow.

The best way to determine exactly what fees you’ll pay is to find a lender and pre-qualify for a mortgage. This process will allow a borrower to receive a loan estimate from the lender, which will have all of the exact costs associated with the mortgage.

Below I will discuss the steps and most effective ways for an individual to calculate how much they can realistically afford.

* If you need to quickly see how much mortgage you can afford and you do not want to read this entire article, please call me at 619-379-8999 or email me at [email protected].

STEP 1: Calculate Your Monthly Income

To qualify for a mortgage, you and your spouse must prove that you have enough income to cover all of your housing costs, including homeowner association dues and property taxes.

You should also add up all sources of your monthly income, including your spouse’s if you are married, alimony if you are getting some and any other income that you receive.

If you have a fixed-term employment contract or receive a salary from your job, then the calculation is easy. Just add up all of your monthly income and divide it by 12 to get the average amount of money you make each month.

Gross monthly income is the total amount of money earned before any deductions have been made. For example, if you make $45,000 per year and work 40 hours per week, then your gross monthly income is $3,750 ($45,000 divided by 12 months).

If your spouse earns $50,000 per year and works full-time. Her gross monthly income is $4,167 ($50,000 divided by 12 months). Adding these two together gives you a gross monthly income of $7,917 ($3,750 + $4,167).

If you receive variable or irregular income from self-employment, there are several things that you can do. For example, let’s say that you are self-employed and your income varies from month to month or year to year due to market conditions or seasonal factors.

To account for this in the calculation of your monthly income for mortgage purposes, simply average out the last 2 years of your income tax returns and use this figure as your monthly income when applying for a mortgage. These calculations can, however, be slightly tricky because some of the deductions on your tax return are added back into your net income like depreciation, depletion and one-time expenses/repairs.

If you were getting alimony every month or had another source of income such as an investment property, then include that as well. Also include any investments in stocks and bonds or annuities (regular payments) as well as any government benefits.

If you receive Social Security, Alimony, Child Support or any other income source that is Non-Taxable a lender may be able to qualify 25% above what you receive which will allow you to qualify for a slightly higher purchase price/loan if needed.

STEP 2: Calculate Your Monthly Expenses

In addition to this information about your monthly income, lenders will also want to know about your existing debts. This includes credit card debt and any other type of installment loans that you carry each month.

Lenders will take the sum of these debts and add it to your estimated mortgage payment to see if you have enough room in your budget before approving your loan application.

This will include any rent or mortgage, food, transportation, taxes, insurance, and other regular costs of living such as your car payment, credit card payments, utility bills, and other recurring costs.

STEP 3: Debt-to-Income Ratios

Mortgage lenders look at your gross monthly income and your monthly debts to determine how much of a mortgage loan you can afford. This is called the debt-to-income ratio.

Debt to income ratio applies to the comparison of an individuals monthly expenses to their monthly income. Lenders use strict debt-to income ratios when qualifying a borrower for a mortgage, so it is imperative that you get a basic understanding of how this is done.

The housing to payment ratio is referred to as your front-end debt-to-income (DTI) ratio and includes all expenses associated with the mortgage – including principal, interest, property taxes and homeowners insurance. To calculate an affordable front-end DTI, multiply 0.3 by your gross (pretax) annual income, then divide by 12.

In contrast, your back-end DTI is the percentage of your gross monthly income that is applied to all other installment debts (i.e., mortgages, student loans, car payments, credit cards, child support etc). One of the first things to do is itemize all of your debts, including credit card bills, personal loans, and car payments.

The back-end DTI shows the lender exactly how much of your earnings go towards your total debt obligations. Generally, they will look for a borrower with a DTI of around 43-55%. If your DTI is below 43% then you have a better chance of qualifying for a loan.

If your DTI is above 43% then you may have a more difficult time meeting the requirements. FHA mortgages allow a higher number with a front-end DTI of 47% of your gross monthly earnings, and a back-end DTI of 57-59%.

How to calculate your debt to income ratio (DTI)

To determine the size of a mortgage you can afford, your total monthly payment, taxes and insurance (PITI) should not exceed 2x to 2.5x your take-home pay or salary after taxes and other withholding are taken into consideration.

The first step is to calculate your gross monthly income.

To do this, simply figure out how much money you are making each month from all of your documentable sources throughout the year and now divide that by 12. If you are married, figure both incomes into the equation.

Remember I said “documentable”.

If you can’t prove it, it didn’t go into your bank account and or you do not claim it on your taxes, then it is not provable income.

Add up all your monthly debts

Things like a car, credit cards, and stuff that will show up on your credit report are what we are looking for. Figure out what percentage of your income is going towards paying off debts. Generally, figures like 5%, 10%, or 20% are used.

Of course, the lower the better, as you will be more likely to be able to keep up with the payments. So, if your income is $4,000 per month and your debts are $500, this would mean that you are currently at an approximate 13% debt to income ratio.

STEP 4: Calculating Your Mortgage Payments

These are some of the major costs a homebuyer faces when buying a home. Once you have all the costs figured out, you’ll want to sit down with your lender or loan officer to locate a realistic mortgage option.

These expenses include, but are not limited to:

Monthly mortgage payment: Principal, interest, taxes, homeowners insurance (PITI) and HOA dues (if applicable).

Homeowners Insurance

Homeowner’s insurance is required to obtain a mortgage. In fact, you’ll be paying for homeowner’s insurance before you even close on the property. Your lender will require that you pay your first year’s insurance premium when you close on your home loan, and it will be included in your monthly mortgage payment.

Homeowners insurance covers the structure of your home and your personal property inside, up to the policy limits. Most policies also cover liability and additional living expenses if something happens to your home.

For example, if a tree falls through your roof or an electrical fire damages half of your house and you can’t stay there for several months while it’s being repaired, homeowners insurance would cover the cost of temporary housing until your home is again habitable.

How much does homeowners insurance cost?

The typical homeowners policy costs between $1,000 to $5,000 per year, depending on where you live. Premiums vary based on factors like location, coverage limits and replacement cost value (RCV) as well as high risk areas for fire or natural disasters.

In general, if you have a $100,000 mortgage on a house that’s worth $550,000 (the value of the house is also called the replacement cost), your lender requires that you have at least $450,000 in liability coverage and $550,000 in coverage for the structure itself. In addition, you’ll want to protect any personal items inside the home with a rider or floater policy.

The more coverage you take out, the higher your premium will be.

Interest Rate

The two main variables that you will have to consider when determining how much you can afford are the loan amount and your interest rate.

Home loans are typically broken up into two types:

Fixed-rate mortgages have an interest rate that is set and does not change for the length of the loan. This provides stability, but if interest rates go down you will miss out on the lower rate. The most common fixed-rate mortgage is a 30-year loan.

Adjustable-rate mortgages (ARMs) start out with a low, fixed rate and then adjust upward or downward after a certain period of time, depending on market conditions at that time. Most ARM loans provide a fixed-rate payment for three to five years and then adjust every year thereafter.

These are also called 3/1 and 5/1 ARMs, which means they start with a fixed-rate and payment for five years, then adjust annually after that.

Private Mortgage Insurance (PMI):

If you do not have a 20% down payment to purchase the home, you will more than likely be subject to paying PMI. If so, this cost will be figured into your monthly mortgage payment.

You pay PMI as part of your monthly mortgage payment until you reach at least 20 percent equity in your home,, but there is no obligation for your lender to do so. This can take quite some time, especially in a rising real estate market where the value of the home increases faster than you can pay down your loan.

PMI can cost between 0.3% to 1% of the original loan amount on an annual basis. That means that if you borrowed $200,000, you may be paying as much as $2,000 a year — or around $167 per month — assuming a PMI rate of 1%.

There are different ways to eliminate mortgage insurance with less than 20% down; you can buy it out as a single premium, which is a lump sum at closing, or through an option called lender paid, which is a less common direction where you would have a higher interest rate that covers the cost of the premium.

Real Estate Taxes:

Real estate taxes are simply the taxes you pay for your home. All residential property requires the homeowner to pay property taxes – prices will vary from city-to-city, state-to-state.

Each town and county sets their own tax rate and the assessor determines the property value. This information is provided to you by your mortgage company, but you may also contact the local tax assessor’s office to confirm or to find out other important information.

Taxes may be paid annually, twice a year or quarterly. Most of the time when you put less than 20% down the lender will require you to include your taxes and insurance with your mortgage payment. In addition to property taxes, some municipalities also charge a municipal tax or supplemental tax – which is usually a fixed amount that doesn’t change year-to-year.

Down payment:

A down payment is required to purchase real estate. The down payment is subtracted from the purchase price of your home. Your mortgage loan will cover the rest of the price of the home.

The minimum amount you’ll need for your down payment depends on the purchase price of the home you’d like to buy and the type of mortgage.

Most conventional loans will require at least 20% down to obtain favorable terms and avoid private mortgage insurance (PMI) however many borrowers choose to only put 3-5% down in today’s market.

Some lenders offer special programs for buyers, however, which may lower the amount needed for a down payment. FHA loans, for example, may allow buyers to qualify with only 3.5% down if they have a credit score of 580 or higher. Down payment assistance programs may be available for buyers in certain areas who meet income qualifications.

In addition to the down payment, you will also need cash reserves on hand to cover closing costs and repairs that come up during the home inspection process.

Closing Costs:

In addition to a down payment, lenders and third parties associated with the transaction will charge fees to close the loan.

These fees may include loan origination fees, credit report fees, attorney fees, appraisal fees, underwriting fees, etc. In general, borrowers can expect to pay approximately 2-4% of the purchase price in closing costs.

While most of these closing costs must be paid by the borrower, some of them can be paid by the seller, split between buyer and seller or even credited by the lender. It is important that you ask your lender what costs are negotiable and which ones are non-negotiable before making an offer on a home.

Points:

Mortgage points are an upfront loan cost that could save money throughout the life of your loan. Mortgage points can be purchased in order to lower the overall interest rate on your loan. A lower interest rate means lower monthly payments as well as less money being paid over the life of the loan.

The cost of a point is 1% of your total loan amount. For example, if you’re borrowing $500,000 to buy a home, each point will cost you $5,000. Usually every 1% paid to buy the interest rate down equates to .25% in rate.

If you are planning on living your home for a long period of time and expect interest rates to rise, it can be a very wise idea to consider that is also typically a tax-deductible expense, of course consult with your accountant or tax professional the impacts to your taxes when you purchase a home.

Bonus Tips

It is always good to undershoot the number you can most afford. It is better to buy a cheaper house and to have extra money, than it is to overdo it and come up short.

Use a mortgage calculator to determine how much you can afford

Lenders tend to use a formula that is very complex to help decide how much a borrower is able to afford. By using a mortgage calculator you will be able to decide for yourself how much you can afford to pay by factoring in your income, debt, and other expenses to see if you qualify for a home loan.

You can start by calculating your gross income on a monthly basis. Then, you can use a mortgage calculator to determine how much house you can afford.

Here are a couple of sites that offer free calculators: Mortgagecalculator.org or Mortgagecalculator.net

These tools will allow prospective home buyers to get a good estimate as to what their monthly mortgage payments should be.

But be aware that this tool will only be able to give an estimated amount, so it would be wise to speak with a mortgage counselor to get concrete numbers.

Interest rates and guidelines may also vary from lender to lender, so it is always important to first shop around for the best deal before you make your purchase. And in the end, the mortgage lender will have the final say as to how much the monthly payment will be.

If you would like to know exactly how much mortgage you can afford, please call me at 619-379-8999 or email me at [email protected].

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Mar 29, 2022 | Mortgage Help |

If you do not have a 20% down payment to purchase the home, you will more than likely be subject to paying private mortgage insurance (PMI), which will be figured into your monthly mortgage payment.

PMI protects the lender in case you default on your loan and don’t have enough equity built up to sell the home and pay off the loan balance. Private mortgage insurers are for-profit companies that provide this protection for lenders.

Private mortgage insurance (PMI) is an extra mortgage cost that is used to cover the risk to a lender, and that is paid by a borrower in monthly premiums tied into their mortgage payments. It is not for the benefit of the borrower.

This type of insurance is usually required by lenders when a mortgage loan amount is above 80% loan to value (LTV) and the borrower has less than a 20% cash stake in the property. A loan amount above 80% is considered a lot riskier to lenders, and in order to cover this risk, they require insurance that will pay them in case the borrower defaults on the loan.

PMI payments range anywhere from 1% to as high as 1.5% of the loan amount that is amortized yearly and paid monthly throughout the life of their loan as long as the loan amount is above 80%.

For example, let’s say you get a $100,000 loan amount and are required to have mortgage insurance. Your estimated monthly insurance payments would be approximately $100 extra a month. A $200,000 loan amount would equate to approximately $200 a month in extra insurance fees.

As you can see, this money can add up quickly. Also, please keep in mind that this money does not help pay down the mortgage balance, and it is not tax-deductible.

You pay PMI as part of your monthly mortgage payment until you reach at least 20 percent equity in your home.

Because PMI exists for the benefit of the lender rather than the borrower, it would make perfect sense that most borrowers would be curious about either avoiding or canceling their PMI policies in order to save money on their monthly payments.

Although it is possible to eliminate the need to pay for PMI, the money required and process can be difficult for many people.

Here are a few ideas on how to avoid private mortgage insurance (PMI).

1. Make a 20% down payment

The most commonly known way to avoid private mortgage insurance altogether is to make a full 20% down payment when closing on your mortgage.

By putting 20% down, the lender knows you are a serious borrower who is placing a good chunk of money as a down-payment and they only have to extend an 80% loan, which makes it considerably less risky. This is also called an 80% loan to value.

Making anything below a 20% down payment automatically binds a borrower to a PMI plan.

However, having 20% down is easier said than done, and many borrowers are unable to meet this demand. This makes this specific method difficult for a lot of people.

2. Get a Second Mortgage

Another way to avoid the PMI policy would be to take on one of these funny-named loans, also known as “80-10-10” or “80-5-15” mortgages. The secret of this loan lies with the fact that it is actually two instead of one.

Although the thought of two separate loans on one mortgage plan might sound scary, they actually reduce the amount that you have to put down on a home while still avoiding PMI. Someone with just enough cash to make a 10% down payment is going to get a 90% mortgage and be stuck with a PMI premium.

Piggyback loans allow home buyers to take on one mortgage for 80% of the purchase price, and a second for 10% of the purchase price.

Under the program, the two loans make one mortgage at 90% of the purchase price, but act as two separate finance options. That 10% down payment under this program will suffice for the 80%-10%-10% plan, and could end up being even lower at 5% for the 80%-5%-15% plan.

Under this option, the 80% loan will not require PMI, and most lenders who hold this plan won’t require PMI under it due to the smaller lower-risk loans. Like everything else, piggybacks come with their downsides.

For example, the interest rate for the second loan will most likely be higher due to such a short term. While paying it off, you may end up paying a little extra in interest, all to save yourself from PMI.

3. Wait for your equity to rise above 20% loan to value

If you are currently paying mortgage insurance, the only way to cancel the insurance is to have more than 20% equity in your property. Some people will need to build equity over time if the housing markets allow them to eliminate their insurance policies. If your homes increase in value so you have 20% equity, then you can have the insurance canceled.

This will not happen automatically.

You have to call your mortgage servicers and have them review your mortgage and home value to assess if you can have the PMI requirement waived.

Important note:

Please keep in mind that mortgage insurance is not an insurance policy to protect you in case you miss your monthly mortgage payments, but for the lender only. If you fall behind on your monthly payments and you have this type of insurance, you can still lose your home to foreclosure.

It is your lender who would benefit from the insurance because they would still be paid in full even if you stopped making mortgage payments altogether and/or if you were foreclosed on.

To see if you’ll be paying PMI, you can start by talking to your loan officer about the details of your loan. They’ll be able to look at the specifics and let you know the amount you will be paying.

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Oct 3, 2021 | Mortgage Help |

If you are unable to pay your mortgage, refinance, or get a loan modification, you may be able to qualify for what is called a “deed in lieu of foreclosure.”

A deed in lieu of foreclosure (DIL) is a legal procedure in which you willingly transfer your property’s title (deed) back to the lender.

In return, the lender agrees to release you from all legal obligations to the mortgage contract. This will be done to satisfy a defaulted loan and to prevent foreclosure proceedings.

A DIL is often better than just walking away from your home and letting it fall into foreclosure because it has a less detrimental effect on your credit score.

You can also negotiate with your lender so that they will not legally come after you to collect any money you may owe on the mortgage in back payments and fees after the lender has sold the property.

On the other hand, a deed in lieu is also beneficial for the lender because it avoids the costs and effort required for a foreclosure sale.

What are the elegibility requirements?

You may qualify for a DIL but let me warn you that this is not an easy process. Before your mortgage servicer even considers this option, you must meet specific elegilibility requirements;

- You cannot afford your current monthly mortgage payments

- The property must be your primary residence, not an abandoned or investment property.

- You’re experiencing financial hardship, such as losing your job, reduced income, significant illness, divorce, or another difficulty.

- You’re unable to obtain a loan modification and have exhausted all other loan workout options and financial resources available to you.

- You tried to sell your property with a licensed real estate brokerage at fair market value for at least 90-120 days but were unsuccessful

- You don’t wish to stay in your house due to other circumstances, such as a job relocation

- You must have actively explored and exhausted all other options and financial resources available to you.

How do I get a deed in lieu of foreclosure from my lender?

In general, a deed is a right granted by a legal contract based upon mutual agreement; therefore, a deed-in-lieu must be based upon voluntary agreement in good faith.

To proceed with a deed in lieu, both parties must agree to and sign both an Agreement in Lieu of Foreclosure, which outlines the terms of the deed and the deed itself, which transfers legal ownership of the property.

For the agreement to be reached, the property’s appraised market value must be less than the original agreement’s outstanding debt, and the property must not be subject to any 3rd party creditor claims or liens.

A third party escrow service then executes the legal agreement, which will release both you and the lender from the original contract.

Once the agreements are reached and there a clear title, the lender then classifies the original loan as paid and issues a waiver to a deficiency judgment. This will typically go into effect if the property’s sale results in less than what is owed on the debt.

Please be advised that many lenders may not be amenable to a deed in lieu because they believe they will have a better title after a standard foreclosure sale. This is because a trustee’s deed of sale effectively erases any judgment liens and second and third mortgages after a foreclosure. Thus, it would depend on the borrower’s lender whether they will accept a deed in lieu or not.

How will it affect my credit?

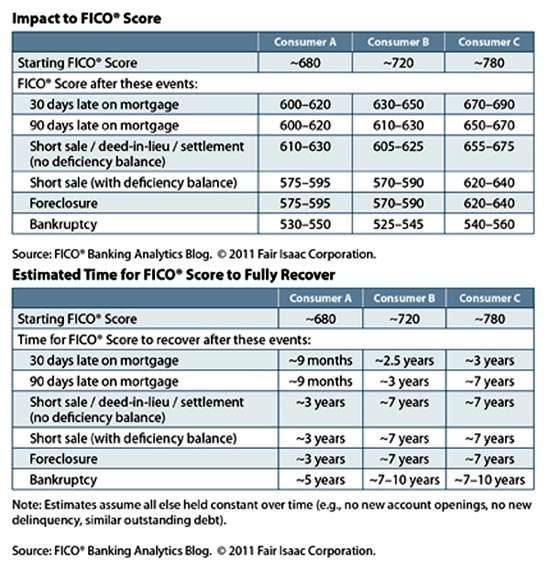

A deed in lieu of foreclosure will cause a negative impact on your credit score. According to a 2011 FICO study, if you begin with a score of approximately 720, it will drop 105 to 125 points off your score; but if you start with a score of 680, you’ll lose 50 to 70 points. But please be aware that your score will drop a lot more if there is any deficiency balance owed.

Here are the charts from FICO;

With that said, you can expect to lose from 50 points minimum to 250 or more points depending on your credit score when you started and if you own a deficiency balance or not. The credit report will also reflect the deed in lieu for seven years, although a borrower can still rebuild their credit.

However, the ill effect on the credit score gradually lessens in time, and you may request its removal from a credit report towards the closing of year seven.

Tax Consequences

Please be aware that if you can complete a deed in lieu of foreclosure, you will still be liable for taxation on the cancellation of indebtedness or COD income. The tax results would be based on whether the loan is classified as a non-recourse loan or a recourse loan.

You can find out if your loan is recourse or non-recourse in your original loan documents that were initially signed by the lender and borrower.

A, if the basic rule of thumb is that if a lender’s only option is to take possession of the property when the borrower defaults, it is a non-recourse loan. However, if the lender can go after the borrower to collect any shortfall when the property is sold, then it is a recourse loan.

A lender will submit a Form 1099-C to the IRS in the case of a shortfall. This is known as the borrower’s COD income.

In the case of a non-recourse loan, the IRS will consider the deed’s tax consequences in lieu as if the borrower had sold the property. If the property’s current market value is less than what is owed, the borrower will have a personal loss, but this is not tax-deductible.

On the other hand, if the property’s value is greater than the outstanding loan, the borrower will have a gain that may not be taxed if he is able to comply with IRS Sec. 121 two-year residency requirement. In the case of a recourse loan, the situation is similar to the non-recourse loan except that the borrower will also be taxed for COD income if the property’s value is less than what is owed. Ordinary income rates will be applied for the COD income.

According to the IRS, the amount of the benefit must be reported as income received under IRC §61(a)(11)3, unless the taxpayer qualifies for an income exclusion under IRC §108.

When can I buy another home?

Most lenders will not offer a loan to a borrower who has filed a deed in lieu for a minimum of two to three years since it will significantly bring down your credit score. The chances of loan approval increase after a few years, especially if a borrower attempts to rebuild their credit score.

But please be aware that some alternative lenders may extend a mortgage to borrowers who maintain good credit score (680 and above) with large down payments in the 25-30% range.

Generally speaking, you will have to wait after a few years as passed and new credit has been established to purchase a home once more.

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Oct 3, 2021 | Mortgage Help |

The CARES Act was designed to help struggling homeowners during the COVID pandemic by offering mortgage forbearance options. Millions of homeowners took advantage and didn’t have to pay their mortgage for three months or longer, depending on the lender.

Now that the forbearance period has ended, many homeowners still need help. If you have a mortgage owned by Freddie Mac or Fannie Mae, you may be eligible for a Flex Loan Modification.

Please keep reading to learn what it’s all about.

How to Get a Flex Loan Modification

Any borrower who is 60 days or more past due on their mortgage or in an imminent default risk may be eligible for the Flex Loan Modification. This new program replaced the previous Home Affordable Modification Program and is only for borrowers with a Freddie Mac or Fannie Mae Loan.

To qualify, you must meet the following:

- You’re experiencing an eligible hardship that affects your ability to pay your mortgage

- You don’t have enough money to cover the mortgage payment and taxes/insurance as it stands

- You have a stable income that allows you to pay the modified mortgage

- You must have originated the mortgage at least 12 months before the request for a loan modification

- You aren’t eligible for a refinance or relief refinance based on your financial situation

- A relief option, such as breaking up the past due amount over a series of months, isn’t feasible

The loan also must not be in the middle of any assistance or recourse, including any workout options, forbearance plans, or active trial plans.

You also must not have modified the mortgage more than 3 times in the past or have failed a past trial period within the last 12 months.

If you’re eligible, you must provide all documentation for a Borrower Response Package, including:

- A completed and signed Uniform Borrower Assistance Form

- Documentation of your hardship

- Proof of income to show that you can afford the loan

Some borrowers may be eligible for a streamlined program if they:

- Are more than 90 days past due and in imminent danger of foreclosure

- Have a step-rate mortgage and become 60 days or more past due within the first 12 months of the interest rate change date

If you’re eligible for a streamlined modification, you don’t have to complete the Borrower Response Package. The lender can modify your loan immediately to avoid the risk of foreclosure.

What Does the Flex Modification Program Offer?

Eligible borrowers may get a more affordable mortgage payment so they aren’t at risk of losing their home.

Lenders have a few options when modifying your mortgage, including:

- Adjusting your interest rate

- Extending your loan term

- Adding the past due amount to the back of the loan and re-amortizing your loan over the new extended term

One final option is setting up a forbearance agreement for part of the loan (usually the amount past due). The lender would then amortize the loan using the current balance without the past due amounts, and the past due amount would become a balloon payment that’s due at the end of the loan. So if you keep the loan for the entire term, your final payment would be the full amount of what is due.

What are the Benefits?

Eligible borrowers experience many benefits with a Flex Modification including:

- Your home loan will be current once you pass the trial period.

- You won’t have to worry about losing your home if you remain current on your new payments.

- Your payments may be as much as 20 percent lower depending on how the lender adjusted your loan.

Do you Need to Apply?

If you are 60 – 90 days behind on your mortgage, you can apply for a Flex Modification if Fannie Mae or Freddie Mac owns your loan.

But, lenders are required to offer the program to any borrower who is 90 days to 105 days past due. So if you are late on your mortgage, you may see this offer from your lender. It won’t tell you the details of the arrangement or what you qualify for, but they will offer you the chance to check your loan and the possibilities to modify it.

By law, if you apply for a modification more than 37 days before your home goes into foreclosure, the foreclosure proceedings must stop. The lender may process your request for a modification, and they start foreclosure proceedings again unless you don’t meet the requirements for a modification.

Passing the Trial Period

All borrowers who get approved for the modification program must go through a trial period. It usually lasts 3 to 4 months. The lender uses this time to make sure you can afford the payments. You must make the payments on time to ‘pass the trial period.’ If you don’t pass, your loan reverts to its original state, and you risk losing your home.

If you make the payments on time, though, the modification replaces your original mortgage and you have a new payment.

Get Help if You’re Struggling

If you’re struggling to make your home loan payments, ask for help. Most lenders are offering the program that has helped millions of borrowers keep their homes while making their loans more affordable.

It’s essential to contact your lender as soon as you know you’re struggling.

Don’t wait and let the home go into foreclosure.

If you wait too long, it could leave you without any options. Discuss your options with your lender, ask as many questions as you need, and figure out the plan to help you keep your home during these trying times.

To get free help online, visit our online mortgage forum at this link.

For those out there who need some housing counseling, please visit the Consumer Financial Protection Bureau’s (CFPB) “Find a Counselor” tool to search for counseling agencies in your area.

Call the HOPE™ Hotline at (888) 995-HOPE (4673) or for other mortgage and financial resources, visit: https://www.consumerfinance.gov/coronavirus/

Or visit HOPE NOW and Neighborhood Assistance Corporation of America (NACA).

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Erik Sandstrom | Aug 18, 2021 | Mortgage Help |

On July 30, 2021, the Federal Housing Administration (FHA) announced an extension of its moratorium on evictions for foreclosed borrowers and their occupants through September 30, 2021, in response to COVID-19 and the ongoing economic recovery.

FHA’s eviction moratorium extension will also help ease some pressure from lenders who are seeing a rise in delinquencies as rates climb higher.

As part of the COVID-19 Forbearance Plan, Mortgage servicers cannot initiate evictions for FHA Single Family Title II forward, and Home Equity Conversion Mortgage (HECM) foreclosed properties unless they are legally vacant or abandoned.

The initial forbearance period may be up to six months and an additional period of up to six months may be requested by the Borrower for a maximum of 12 months and must be approved by the Mortgagee. The forbearance must not extend beyond June 30, 2022.

“We must continue to do everything within our authority to make sure that foreclosed borrowers who are impacted by the pandemic have the time and resources to secure safe and stable housing, whether it’s in their current homes, or by obtaining alternative housing options,” said Principal Deputy Assistant Secretary for Housing Lopa P. Kolluri.

“We don’t want to see any individuals or families displaced unnecessarily while trying to recover from the pandemic.”

Mortgage servicers may initiate or continue foreclosures following FHA requirements once the moratorium expires.

Hi. my name is Erik Sandstrom. I’m LoanSafe.org’s mortgage expert and a senior loan officer with Prime Lending.

If you need a live rate quote, or need help getting a new mortgage, please call me anytime at 619-379-8999 or by email [email protected].

by Erik Sandstrom | Aug 9, 2021 | Mortgage Help |

The documents required for a mortgage refinance will vary depending on the lender you use. If you stick with your current lender, chances are they still have a lot of your information already on file. However, much of this information will change over the years and will most likely be updated.

It also depends on the lender you apply with and the type of loan you apply for, and understand that with the information you provide, you must also provide all necessary documents to prove that income.

The basic items you will need to refinance are your latest two years of tax returns, six months of bank statements, and pay stubs or proof of income.

Some lenders might require pay stubs over another form of income. With bank statements for various bank accounts, you’ll usually have to obtain the most recent 2-3 months of statements, including the account names, addresses, account numbers, and balances.

Other lenders may even request your diplomas and transcripts and f you are receiving a gift from someone, you must bring a copy of the gift letter.

You will need to know your existing mortgage loan balance for payoffs and payments verification. You can call your lender for an updated statement.

Here is a list of the general items and documents you will need to refinance your mortgage:

– Photo ID and social security number

– Proof of income (copy of paycheck over last 30 days or employer contact info for last 1-2 years). Self-employed borrowers must provide year-to-date profit and loss statements or balance sheets. Pension plans, social security, alimony, and rental property statements also qualify for legitimate income sources

– Tax forms (W-2s and 1099s), are generally required for each loan applicant. Self-employed borrowers must have signed tax returns from the previous 2 years

– Financial records of debts such as student loans, car notes, child support, alimony, insurance, and tax bills

– A homeowner’s insurance policy

– Bank statements for checking accounts, savings accounts, credit union accounts, mutual fund accounts, retirement plans statements, 401K forms, and any other assets

– Statements for mutual funds, bonds, and other securities

– Copy of the deed to your property

– Copy of title insurance

– Loan-to-value appraisal: Most lenders will accept informal appraisals and estimates of relevant figures, but others will require a formal analysis.

– A list of your addresses of residences for the last two years.

– Copy of purchase agreement (If a new construction loan, you may need to provide copies of plans and specifications)

– If you are a resident alien, evidence of permanent residency issued by INS (Green Card)

Hi. my name is Erik Sandstrom. I’m LoanSafe.org’s mortgage expert and a senior loan officer with Prime Lending.

If you need a live rate quote, or need help getting a new mortgage, please call me anytime at 619-379-8999 or by email [email protected].

by Moe Bedard | Aug 5, 2021 | Mortgage Help |

To qualify for a loan workout such as a loan modification, short sale, or forbearance, you as the property owner must write a hardship letter to your lender to prove that you are facing financial difficulties. The purpose is to explain the details of your financial situation and the reasons why you can no longer afford your mortgage payments and detail the steps you are taking to correct your problem.

Having a well-written hardship letter is one of the most critical steps in getting your request approved. In this article, we will explain how to write one and give you a couple of examples that you can use as a template for your own letter.

When writing your letter, it’s essential to understand what your lender wants to hear. They want you to write out a solution that makes sense and will help you afford your payments and stay in your home.

You can let them know what you feel you can afford each monthly payment or even what modification programs you think you may qualify for. This will make your lender aware that you are ready to take on a new affordable loan and continue paying your monthly payments.

It would help if you remembered to be as honest as possible because your lender will also require all of your financial information and run a credit report. If your lender finds that you have lied about your financial situation, your request will automatically be denied.

Also, make sure that your letter is not too long and straight to the point. You do not want to write a 3-4 page letter because most reps will not take the time to read the entire letter. Remember that mortgage servicers and lenders are entirely overwhelmed with requests because of the current economic crisis.

EXAMPLE HARDSHIP LETTERS

Eligible hardships include job loss, income reduction, illness, relocation, divorce, medical bills, death of a spouse, etc. In your letter, you will also want to note when each event occurred and include any documentation that you can. For example, if you recently lost your job, you will want to show that you have a new job or are actively searching for employment.

Here are some examples that lenders will consider:

Divorce

Reduced Income

Loss of Job

Illness

Death in family

Military Duty

Incarceration

High Medical bills

Significant damage to property(such as vandalism or natural disaster)

Now that you know what hardships your lender is looking for, you are now ready to begin writing your own. But keep in mind that this is only one factor of the loan workout process. Your lender will not automatically assist you just by reading your letter, and there will be many other factors involved as well.

Here are two example letters were written by real homeowners and members of the LoanSafe forum who had received a loan modification from their efforts.

Name: (Your Name)

Address: (Your Address)

Lender Name: (Your Lender)

Loan #: (your Loan #)

To Whom It May Concern:

We are writing this letter to explain the extreme financial hardship it will be for our family when our loan adjusts from a 7.75% interest rate to a 10.75% interest rate in August 2020. This interest rate adjustment will cause our payment to dramatically increase in the amount of $1695 per month on top of our current payment of $4234.10, increasing the payment to $5929.10 per month. Our current income does not support an increase of this magnitude. As a matter of fact, a monthly increase of this amount will ruin us financially, and within a few short months of this adjustment, we will surely fall into foreclosure as we will not be able to afford the monthly payment.

We conducted a counseling session with a woman named Deborah Winston (888-669-2227 x742) from 995-HOPE and submitted a monthly budget where we only have a surplus of $158 per month after we pay all of our monthly obligations. According to the counselor, we are currently utilizing 54% of our monthly income for housing costs which is way above the national average.

My husband, Kevin, is the bread winner in the family and his income varies from paycheck to paycheck because of overtime, holiday pay (2 times per year), and uniform allowance. So, sometimes he makes his base pay of approximately $7839 per month and other times he makes more than that depending on the overtime he works each month. However, overtime is never guaranteed, so we cannot depend on the overtime in order to fulfill our monthly obligations.

I am currently receiving Social Security Disability in the amount of $1435 and am also the payee for our son, Christian, in the amount of $717 per month. Also, I receive a check from Calpers for my disability retirement in the amount of $829.74.

We would appreciate the opportunity to work out a loan modification where our interest rate will be frozen at the 7.75% interest rate for the DURATION of the loan, if the rate is just frozen for 2 to 5 years we will find ourselves in the same situation in a few short years from now.

Please take the time to review the information we submitted and consider our request. It is very important to us that we keep our account in good standing and preserve our credit rating as well as protect our main asset….our home.

Thank you in advance for your time and consideration in this matter. We are looking forward to working with Option One to resolve this situation. If you have any questions please contact us at xxx-xxx-xxxx.

Sincerely and Respectfully,

Borrower’s Signature

Date

Co-Borrower’s Signature

Date

————————————————————————————————————————————-

Sample Hardship Letter #2

Name: (Your Name)

Address: (Your Address)

Lender Name: (Your Lender)

Loan #: (your Loan #)

To Whom It May Concern:

I am writing this letter to explain my unfortunate set of circumstances that have caused us to become delinquent on our mortgage. We have done everything in our power to make ends meet, but unfortunately, we have fallen short and would like you to consider working with us to modify our loan. Our number one goal is to keep our home, and we would really appreciate the opportunity to do that.

There are several reasons that caused us to fall behind on our payments:

a) On July 6, 2019 my husband, was laid off from his job with IBM. He no longer receives Unemployment Compensation from the State of Florida as of January 2020.

b) Since July 2019, we went down to one income and were unable to keep up with the higher mortgage payments due to our escrow account from the beginning of 2019 being short on funds due to raised taxes and insurance coverage in Flagler County, FL.

c) In November 2020, we had to fly out of State for a family emergency which did not enable us to make that months payment.

d) Since we no longer have medical coverage, I had to pay for my visits to the doctor on several occasions due to prolonged and excessive menstruation. The Doctor Office would not see me unless I had full payment at each visit.

e) Since there is only one income in our household, but my husband helps me with my business while still looking for a comparable job, I must travel a lot. Gas prices have become extremely high, if I do not travel to do presentations and meet with clients, I cannot assure growth.

It feels like catch up for those two months we fell behind on is almost impossible, I assure you we have every desire of retaining our home and repaying what is owed to Bank of America. But at this time we have exhausted all of our income and resources, so we are turning to you for help.

Our situation is getting better because, like I stated above, my husband and I have combined forces, and we are working my business together in order to ensure stability and growth in our income, and we feel that a loan modification would benefit us both. We would appreciate if you can work with us to lower or delinquent amount owed and/or our mortgage payment so we can keep our home and also afford to make amends with Bank of America.

We truly are looking forward to you working with us, and we are anxious to get this settled so we all can move on.

Sincerely and Respectfully,

PLEASE JOIN THE LOANSAFE FORUM!

You can find more examples of various hardship letters right here written by different homeowners in the LoanSafe forum. =

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.

by Moe Bedard | Aug 5, 2021 | Mortgage Help |

A loan modification changes your current mortgage contract, such as a reduced interest rate or extended loan terms agreed upon by the lender and the homeowner.

For homeowners struggling to manage or behind on their current mortgage payments, a loan modification will probably be the best option to help your current situation. The purpose is to help make your mortgage more affordable so you can avoid foreclosure.

For example, the lender modifies the existing loan(s) to work with the homeowner because of financial hardship by changing the mortgage terms from an adjustable-rate mortgage (ARM) to a fixed-rate loan. They may also extend the loan term from 30 to 40 years or decrease the current interest rate to make the monthly payment more affordable.

Every mortgage servicer in the U.S. has loss mitigation programs in place and offers loan modifications to borrowers who they deem are qualified. But please keep in mind that they are not required to modify your mortgage, and there are no laws that state they must fix your loan so you can save your home.

A key factor required in every loan modification submission is the existence of hardship. The hardship can be temporary in nature or permanent. Still, the borrower must prove the hardship such as financial hardships, job loss, loss of income, rate adjustments on adjustable-rate and subprime mortgage products, etc.

The earlier you address the issue, the better the chances of negotiating a fixed rate and a manageable payment.

What are the types of hardships?

The following list are a sample of hardships that are deemed acceptable by mortgage servicers

1. Adjustable Rate Mortgage – Reset-Payment Shock

2. Illness of the Borrower

3. Illness of a Borrower’s Family Member

4. Curtailment of Income

5. Loss of Job

6. Property Problems

7. Inability to Sell the Property

8. Mortgage Servicing Problems

9. Reduced Income

10. Failed Business

11. Job Relocation

12. Death of the Borrower

13. Death of Spouse or Co-Borrower

14. Death in the Family

15. Incarceration

16. Divorce

17. Marital Separation

18. Military Duty

19. Medical Bills

20. Damage to Property (natural disaster or unnatural)

How does the process work?

A loan modification is simply done by negotiating a lower payment with your current lender on your current mortgage contract.

The process works by modifying and improving the current terms and/or the interest rates on your existing mortgage. Do not confuse it with refinancing because you would not be making payments to satisfy an existing loan; this means that there are no loan closing costs.

It can easily take anywhere from three to twelve months or more to complete, and in some cases up to two years or more. Even if you feel like you’re a perfect candidate for a loan modification, you will most likely have to jump through several hoops before you reach success.

Just try to always be very polite – but firm – each and every time you communicate with your servicer. Keep track of dates/times and the name of any representative you speak with, this may come in handy later if you get conflicting information from a separate department.

The key when applying for a loan modification is to have patience and be persistent. This process may take a long time and be stressful. Try to control this stress and understand that what you cannot control is not good to stress over. This is just business to these big banks and mortgage servicers. If you remember this and do the same yourself, it will help you deal with the stress and sometimes the comedy of it all.

Do the best you can, stay as positive as possible, and hope for the best. By doing this you will take care of business, and also have a life with your loved ones.

What will I need to apply?

Here is a list of items you will need when you submit your loan modification. It is best to gather all these items before you even approach your mortgage servicer and keep this paperwork all organized in a single file for quick reference and or updating.

1. Financial statement

This worksheet can be defined as a document that contains a borrower’s monthly income and expenses that they wrote down. Accuracy of the information on this worksheet is a major factor in eligibility. The absence of debts may disqualify you, due to the fact that your servicer is going to uncover them eventually whether they are on the document or not.

2. Hardship letter

As mentioned above, hardship letters help to outline the events that have led to your mortgage becoming unaffordable. Although crucial information needs to be addressed in this letter, it also needs to be straight and to the point. Using over 2 pages to describe your situation is actually overdoing it.

3. Proof of income

Usually, income must be verified for each borrower who lives in the primary residence. Evidence of income classifies as:

– Monthly pay stubs for salaries of hourly wages.

– Most recent quarterly profit and loss statements of the self-employed.

– Copies of statements or letters from providers of the unemployed or disabled who need federal benefits to live. The statements or letters should include how long you will be receiving the benefits or the 2 most recent bank statements proving the income.

– The copies of the divorce decree, separation agreement, or other agreements in writing filed with the court explaining how much you will be paid and the amount of time in which it will be received for those who receive alimony or child support.

4. Tax Authorization (IRS 4506T-EZ Form)

Your lender needs this form for permission to request a copy of your most recent tax return from the IRS. Borrowers should make copies of this form for their own records.

5. Bank statements

At least two months of bank statements are required when applying for a loan modification. Bank statements enable a lender to see your total income and expenses and how they are being distributed each month. This transparency will help them make their decision. It is common to have to send in statements multiple times during the process, so trying not to get frustrated.

Here are some more tips to help you along in the process

1. Being punctual

Instead of waiting to default on your monthly payments, you could contact your servicer’s loss mitigation department to apply for assistance. Waiting to get into trouble never helps make a situation better. If you are suffering financially, take action. Patience is a virtue that must be practiced during the loan modification process, not before you even think about submitting the application.

2. Researching

As we promote nearly daily here on LoanSafe, the best way to get the best options is to do your research. While starting at resources like our own forum here on LoanSafe.org can be helpful, the best research always comes from the source. The Making Home Affordable Program, the Freddie Mac Streamlined Modification Initiative, the Fannie Mae streamline, and several other loan modification sources all have websites that anyone can go to for more information.

3. Writing

Hardship letters are always vital tools for borrowers who are facing the reality of foreclosure. While being comparable to hardship evidence, a hardship letter differs in that it sets the stage for a borrower to open up to their lender or servicer and allows them to be honest about their situation. Loan modification and short sale processes generally request it. Sample hardship letters and instructions can be found here on here on LoanSafe.

4. Staying organized

Because all loan modification programs request basic financial information such as paystubs, bank statements, 2 years’ worth of tax returns, recent mortgage statements, and a financial budget you have, the organization is more vital than ever when pursuing a loan modification in 2014.

5. Remaining assertive

When trying to get a loan modification in 2014, you’ll want to remain respectful while at the same time never taking no for an answer. Because the submitting of an application requires constant follow-ups on the phone, it takes the right type of assertiveness of the phone when going after a loan modification. Calling at least 2 times per week will help obtain a positive outcome.

6. Being realistic

Realism does not mean signing the first deal that is presented to you. Bargaining still exists in a world where regulations are ruling the industry. At the same time, remember that those with the power are the ones who make the final decisions; Especially if your loan is owned by Fannie Mae or Freddie Mac.

7. Document everything

This trait falls under the category of staying organized as well. Legal ramifications require borrowers to leave paper trails for themselves in order to get as much help as possible with the least amount of trouble possible. Keeping detailed logs, notes on conversations, and tabs on status updates are crucial tools when pursuing a loan modification this year.

8. Being patient

With some timelines adding up to 90 days to complete, the loan modification process is a process that requires the utmost patience.

IMPORTANT NOTE: It is essential during the loan modification process that you call your servicer regularly after you have sent them all your paperwork. Finding out which department is handling your file is crucial as well.

Where can I find more assistance?

What if I need help negotiating with my lender or do not have enough time to call in weekly for updates?

For those out there who need some housing counseling, I suggest you visit the Consumer Financial Protection Bureau’s (CFPB) “Find a Counselor” tool to search for counseling agencies in your area.

You can also call the HOPE™ Hotline at (888) 995-HOPE (4673) or for other mortgage and financial resources, visit: https://www.consumerfinance.gov/coronavirus/

There are some excellent non-profit organizations out there that can assist you through this difficult process. Two non-profits I have found to be very reputable over the years are HOPE NOW and Neighborhood Assistance Corporation of America (NACA).

Now that you have some information about modifications, it is now time for you to begin the process yourself.

You can also join our free forum with any questions they may have, where you will find many homeowners just like yourself in need of assistance.

Moe Bedard is the founder and lead mortgage analyst for LoanSafe.org. Since 2007, LoanSafe has helped over 2 million consumers with solutions to their mortgage problems and has been featured in the New York Times, LA Times, Fox Business, and many other media publications.