Elon Musk is a well-known entrepreneur and billionaire who is best known for his roles in Tesla and SpaceX.

He has plenty of money, but recently he took out several very large mortgages on five properties in California.

When he borrowed this money, Musk faced some big decisions about which type of loans to go with. There are two options: fixed-rate mortgages or adjustable mortgages.

Fixed-rate mortgages provide the borrower with a guarantee of stable monthly payments.

Adjustable mortgages don’t offer that same benefit, but they do come with substantially lower rates.

Musk chose to take a big risk with his mortgage loans.

Instead of choosing a 30-year fixed-rate mortgage – which would have given him stable monthly payments – Musk chose a hybrid-adjustable loan (ARM).

The Tesla CEO, 49, took out several mortgages worth more than $61 million to buy five adjacent homes in the posh Bel-Air neighborhood of Los Angeles where celebrities like Jennifer Aniston and Kim Kardashian live, according to property records reviewed by Business Insider.

He bought two of the houses – which are located near one another in Bel Air – in 2012 and 2013 for $17 million and $6.75 million, respectively.

Musk bought one of the houses from actor Gene Wilder for $6.75 million, and another from actress Talia Shire for $6.4 million. The other three are located in the Hidden Hills neighborhood of Los Angeles and cost him $24 million combined.

For his new mortgages, Musk secured a floating rate loan with a 3% interest rate for the first six months, which will then increase to 4.5%, according to property records filed with the county recorder’s offices for Los Angeles County, San Mateo County and Alameda County in California.

The loans total $24.6 million from Citibank and $36.3 million from Morgan Stanley.

Musk was able to borrow a high-risk mortgage because he’s a billionaire.

With his wealth, he could afford to take a chance with an ARM mortgage and see his rates go up and payments rise if and when that would happen.

Musk was unlikely to find himself in a position where he couldn’t refinance his loan if needed, especially given his personal wealth and long-established borrowing relationships with major banks.

The typical borrower, however, might not be so equipped to bear the risk of an adjustable-rate mortgage.

The average person would likely find themselves in serious financial hardship if their rates rose — and there’s a good chance they will continue to do so in the forseable future.

The CARES Act was designed to help struggling homeowners during the COVID pandemic by offering mortgage forbearance options. Millions of homeowners took advantage and didn’t have to pay their mortgage for three months or longer, depending on the lender.

Now that the forbearance period has ended, many homeowners still need help. If you have a mortgage owned by Freddie Mac or Fannie Mae, you may be eligible for a Flex Loan Modification.

Please keep reading to learn what it’s all about.

How to Get a Flex Loan Modification

Any borrower who is 60 days or more past due on their mortgage or in an imminent default risk may be eligible for the Flex Loan Modification. This new program replaced the previous Home Affordable Modification Program and is only for borrowers with a Freddie Mac or Fannie Mae Loan.

To qualify, you must meet the following:

You’re experiencing an eligible hardship that affects your ability to pay your mortgage

You don’t have enough money to cover the mortgage payment and taxes/insurance as it stands

You have a stable income that allows you to pay the modified mortgage

You must have originated the mortgage at least 12 months before the request for a loan modification

You aren’t eligible for a refinance or relief refinance based on your financial situation

A relief option, such as breaking up the past due amount over a series of months, isn’t feasible

The loan also must not be in the middle of any assistance or recourse, including any workout options, forbearance plans, or active trial plans.

You also must not have modified the mortgage more than 3 times in the past or have failed a past trial period within the last 12 months.

If you’re eligible, you must provide all documentation for a Borrower Response Package, including:

A completed and signed Uniform Borrower Assistance Form

Documentation of your hardship

Proof of income to show that you can afford the loan

Some borrowers may be eligible for a streamlined program if they:

Are more than 90 days past due and in imminent danger of foreclosure

Have a step-rate mortgage and become 60 days or more past due within the first 12 months of the interest rate change date

If you’re eligible for a streamlined modification, you don’t have to complete the Borrower Response Package. The lender can modify your loan immediately to avoid the risk of foreclosure.

What Does the Flex Modification Program Offer?

Eligible borrowers may get a more affordable mortgage payment so they aren’t at risk of losing their home.

Lenders have a few options when modifying your mortgage, including:

Adjusting your interest rate

Extending your loan term

Adding the past due amount to the back of the loan and re-amortizing your loan over the new extended term

One final option is setting up a forbearance agreement for part of the loan (usually the amount past due). The lender would then amortize the loan using the current balance without the past due amounts, and the past due amount would become a balloon payment that’s due at the end of the loan. So if you keep the loan for the entire term, your final payment would be the full amount of what is due.

What are the Benefits?

Eligible borrowers experience many benefits with a Flex Modification including:

Your home loan will be current once you pass the trial period.

You won’t have to worry about losing your home if you remain current on your new payments.

Your payments may be as much as 20 percent lower depending on how the lender adjusted your loan.

Do you Need to Apply?

If you are 60 – 90 days behind on your mortgage, you can apply for a Flex Modification if Fannie Mae or Freddie Mac owns your loan.

But, lenders are required to offer the program to any borrower who is 90 days to 105 days past due. So if you are late on your mortgage, you may see this offer from your lender. It won’t tell you the details of the arrangement or what you qualify for, but they will offer you the chance to check your loan and the possibilities to modify it.

By law, if you apply for a modification more than 37 days before your home goes into foreclosure, the foreclosure proceedings must stop. The lender may process your request for a modification, and they start foreclosure proceedings again unless you don’t meet the requirements for a modification.

Passing the Trial Period

All borrowers who get approved for the modification program must go through a trial period. It usually lasts 3 to 4 months. The lender uses this time to make sure you can afford the payments. You must make the payments on time to ‘pass the trial period.’ If you don’t pass, your loan reverts to its original state, and you risk losing your home.

If you make the payments on time, though, the modification replaces your original mortgage and you have a new payment.

Get Help if You’re Struggling

If you’re struggling to make your home loan payments, ask for help. Most lenders are offering the program that has helped millions of borrowers keep their homes while making their loans more affordable.

It’s essential to contact your lender as soon as you know you’re struggling.

Don’t wait and let the home go into foreclosure.

If you wait too long, it could leave you without any options. Discuss your options with your lender, ask as many questions as you need, and figure out the plan to help you keep your home during these trying times.

For those out there who need some housing counseling, please visit the Consumer Financial Protection Bureau’s (CFPB) “Find a Counselor” tool to search for counseling agencies in your area.

Homeowners with mortgages backed by Fannie Mae or Freddie Mac are eligible for a two-month extension to avoid foreclosure if they apply to the Homeowner Assistance Fund, according to an announcement on April 6, 2022, by the Federal Housing Finance Agency.

Mortgage servicers will have to suspend foreclosure activities for up to 60 days for eligible homeowners. Assistance can also come in the form of lower mortgage payments and paying utility bills.

“FHFA is committed to sustainable homeownership. Today’s action will provide borrowers who need temporary mortgage assistance with additional time to be evaluated for relief through their state’s approved Homeownership Assistance Fund,” said FHFA Acting Director Sandra L. Thompson.

As of December 31st, there were 178,019 mortgages in forbearance, down from 320,009 in the third quarter, according to an FHFA spokesman, Adam Russel.

Out of the leading states with these mortgages in forbearance, California and Texas ranked number one and three with more than 20,000 and nearly 17,000 mortgages, respectively.

The Homeowner Assistance Fund was created by the CARES Act and is administered by the Treasury Department, provides up to $10 billion to help struggling American homeowners.

Who qualifies for the Homeowner Assistance Fund extension?

To qualify for this two-month extension, homeowners must apply for assistance from the Homeowner Assistance Fund (HAF). The fund covers homeowners who are behind on their mortgage payments due to COVID-19 and don’t have an alternative source of assistance.

Eligible applicants must meet these criteria:

* The homeowner either had a financial hardship caused directly by COVID-19, or they have experienced financial difficulty due to COVID-19 that makes it hard to pay their mortgage.

* They must have a mortgage backed by Fannie Mae or Freddie Mac. To find out if that’s you, go to Fannie Mae’s Lookup Tool or Freddie Mac’s Loan Lookup Tool. Or contact your mortgage servicer directly.

* The original loan must have been sold to Fannie Mae or Freddie Mac before June 1, 2021. Although the loans can be delinquent, they cannot be in foreclosure at least 90 days before applying for HAFA.

* Not already be behind on payments at the time of application.

* Be part of a household with income 80% below the area median income in the location of their property, but only if that amount is no more than $100,000 annually.

* Not have an interest in another residential property at the time they apply for assistance.

The foreclosure moratorium expired on July 31, 2021. However, some states and local governments have temporarily stopped foreclosures.

FHA Loan Qualifications: Learn the guidelines to qualify in 2022 By Erik Sandstrom – To find out the qualifications, guidelines and requirements to apply for a Federal Housing Administration (FHA) loan in 2022, read the guidelines below. This will help you learn...

Rising mortgage rates on FHA loans are driving up monthly payments, making it harder for many to afford.

FHA loans have long been touted as one of the most effective ways for first-time homebuyers to get a mortgage. But with rising interest rates — and a lingering threat of more — FHA borrowers are about to face more pain.

For home buyers, the difference between qualifying for a 3.5% down FHA loan and a 5% conventional loan is significant: about $150 per month on a median-priced home in the U.S., according to one analysis from mortgage data provider CoreLogic.

For people who already have a FHA loan, borrowers will likely see their monthly payments increase due to higher interest rates, which could hurt their financial situation if they don’t have other income streams coming in or an emergency fund set aside in case they lose their job.

If you purchased your home a few years ago, or even just last year when rates were at historic lows, you might be surprised to learn how much higher the rate is today.

The average 30-year rate on FHA-backed loans has risen from 3.97 percent in January to 4.68 percent as of this writing, according to data provided by Ellie Mae, an industry software provider.

That’s a rise of 0.71 percentage points in just six months, and it translates into higher payments for all new FHA borrowers:

$1,429 monthly on a $200,000 loan — an increase of $160 monthly or $1,920 annually

$2,073 monthly on a $300,000 loan — an increase of $239 monthly or $2,868 annually

$2,888 monthly on a $400,000 loan — an increase of $328 monthly or $3,936 annually

Each 1-percentage-point increase in mortgage rates is equivalent to a 10 percent drop in home affordability, according to Trulia.

“FHA buyers are going to get squeezed,” said Jed Kolko, chief economist at Trulia. “They’re going to have higher house payments.”

The rate spike isn’t the only problem facing borrowers with FHA loans right now. Insurance premiums are also expected to rise in coming years — and those increases will hit people who took out their mortgages before the hikes were announced.

The average interest rate on 30-year fixed-rate mortgages increased from 4.20% in March to 4.37% in April, according to mortgage finance agency Freddie Mac (FMCC).

Meanwhile, the average rate on 15-year fixed-rate mortgages rose from 3.43% in March to 3.57% in April.

Just a few months earlier, rates were hovering around 3.5 percent. Homeowners with ARMs are also feeling the pain of higher rates, though the impact will be somewhat less immediate.

The reason for the increase is simple: The Federal Reserve has been raising short-term interest rates as the economy improves and unemployment levels drop.

It’s also winding down its monthly bond purchases that have kept mortgage rates at historic lows.

The Department of Housing and Urban Development (HUD) and the Federal Housing Administration (FHA) are seeking to initiate a new 40-year loan modification program to help mortgage borrowers and lenders streamline the loss mitigation process.

The proposed rule, published by HUD late last week, would change repayment provisions for FHA borrowers, allowing lenders to modify a borrower’s total unpaid loan for an additional 120 months.

HUD said that this option could prevent “several thousand borrowers a year from foreclosure.”

According to HUD, the proposed change would allow FHA lenders to modify mortgages where borrowers experience long-term COVID-19 forbearance due to job or income loss, or where the borrower is subject to an extension of forbearance or additional payment period.

“This will give these borrowers longer periods of time to recover financially before their mortgage payments go back up to their original amount,” said HUD Secretary Marcia L. Fudge.

As part of the plan, if a lender chooses to offer a 40-year modified mortgage to an eligible FHA borrower, the agency will reimburse 100% of the unpaid principal balance owed on the loan at the time of modification. The reimbursement will be made in one lump sum payment upon completion of all terms and conditions in the modification agreement.

HUD also specifies that the monthly payment on a 40-year loan must be no less than the payment on a 30-year loan because it would not want to encourage borrowers to take out loans they can’t afford.

To qualify for the option, FHA borrowers will need to provide documentation demonstrating functionality in their repayment plans and show that they can afford monthly payments based on their current income levels.

Borrowers must also be current on their mortgage payments for at least 12 consecutive months following the modification under this proposal. The proposal is not available for borrowers who are currently in bankruptcy proceedings or who have already had one or more delinquencies within 24 months of their modification request.

In addition, the proposed rule would allow lenders to process loan modifications for delinquent borrowers in cases where they would otherwise be ineligible due to delinquency. Additionally, HUD said that it is considering additional special application and income verification procedures.

“Since March, HUD has been focused on protecting our nation’s homeowners from the financial impacts of COVID-19 through our innovative loss mitigation strategies and programs,” said HUD Secretary Ben Carson. “We believe that this proposed expansion will allow thousands more struggling families to keep their homes and provide them with time to get back on their feet after this challenging time.”

In June, the FHA introduced a new long-term loss mitigation program for borrowers impacted by the COVID-19 pandemic. The new “waterfall” included a six-month forbearance option, the extension of temporary COVID-19 loss mitigation options, and a new permanent FHA COVID-19 loss mitigation option.

HUD said it believes that this proposed change will help streamline loss mitigation efforts for FHA-insured single family mortgages and will ease the operational burden on its lenders. This new option would allow eligible mortgages currently in forbearance or in default due to COVID-19 related hardships to access longer-term modifications.

The FHA is looking to the mortgage industry to help the agency determine if the 40-year loan modification program is a good idea. The agency is currently taking comments from lenders and other interested parties about the current loss mitigation options, including whether or not a 40-year loan mod should be made available.

Figuring out how much mortgage you can afford is a process that involves several steps. Once you have gone through all of them and have thoroughly examined your financial situation, you can have a much better idea as to how big of a loan you can afford, and in turn, how big of a house to look for.

The general rule of thumb is that about a third of a borrower’s income should be dedicated to financing a home. For example, if someone makes an annual salary of $50,000 a year, they should be able to manage a mortgage of $150,000 if their current debt is moderate.

While this tends to be a common rule for some, it will not be the case for every new home buyer.

A good rule of thumb is to examine your current debt, living expenses, and then adjust for future financial obligations, like children, education, and possible retirement.

Instead of trying to spend all your earnings on buying a home, a more modest approach is sometimes necessary. There’s no better way to be well-prepared for homeownership than making a budget and sticking to it!

Aside from considering your regular monthly costs such as utility bills, car insurance, health insurance, etc. – finding out the exact mortgage costs you will be facing will help you determine whether or not the purchase is a sound financial investment.

You also need to keep in mind that a mortgage loan pays not just for your house, but also for the costs of owning a home, such as insurance, property taxes, and home maintenance. All of these things should be factored into your calculations when you are calculating your mortgage.

There are also many more factors such as your interest rate, credit score, debt-to-income ratios and down payment that affect the amount you can afford to borrow.

The best way to determine exactly what fees you’ll pay is to find a lender and pre-qualify for a mortgage. This process will allow a borrower to receive a loan estimate from the lender, which will have all of the exact costs associated with the mortgage.

Below I will discuss the steps and most effective ways for an individual to calculate how much they can realistically afford.

* If you need to quickly see how much mortgage you can afford and you do not want to read this entire article, please call me at 619-379-8999 or email me at [email protected].

STEP 1: Calculate Your Monthly Income

To qualify for a mortgage, you and your spouse must prove that you have enough income to cover all of your housing costs, including homeowner association dues and property taxes.

You should also add up all sources of your monthly income, including your spouse’s if you are married, alimony if you are getting some and any other income that you receive.

If you have a fixed-term employment contract or receive a salary from your job, then the calculation is easy. Just add up all of your monthly income and divide it by 12 to get the average amount of money you make each month.

Gross monthly income is the total amount of money earned before any deductions have been made. For example, if you make $45,000 per year and work 40 hours per week, then your gross monthly income is $3,750 ($45,000 divided by 12 months).

If your spouse earns $50,000 per year and works full-time. Her gross monthly income is $4,167 ($50,000 divided by 12 months). Adding these two together gives you a gross monthly income of $7,917 ($3,750 + $4,167).

If you receive variable or irregular income from self-employment, there are several things that you can do. For example, let’s say that you are self-employed and your income varies from month to month or year to year due to market conditions or seasonal factors.

To account for this in the calculation of your monthly income for mortgage purposes, simply average out the last 2 years of your income tax returns and use this figure as your monthly income when applying for a mortgage. These calculations can, however, be slightly tricky because some of the deductions on your tax return are added back into your net income like depreciation, depletion and one-time expenses/repairs.

If you were getting alimony every month or had another source of income such as an investment property, then include that as well. Also include any investments in stocks and bonds or annuities (regular payments) as well as any government benefits.

If you receive Social Security, Alimony, Child Support or any other income source that is Non-Taxable a lender may be able to qualify 25% above what you receive which will allow you to qualify for a slightly higher purchase price/loan if needed.

STEP 2: Calculate Your Monthly Expenses

In addition to this information about your monthly income, lenders will also want to know about your existing debts. This includes credit card debt and any other type of installment loans that you carry each month.

Lenders will take the sum of these debts and add it to your estimated mortgage payment to see if you have enough room in your budget before approving your loan application.

This will include any rent or mortgage, food, transportation, taxes, insurance, and other regular costs of living such as your car payment, credit card payments, utility bills, and other recurring costs.

STEP 3: Debt-to-Income Ratios

Mortgage lenders look at your gross monthly income and your monthly debts to determine how much of a mortgage loan you can afford. This is called the debt-to-income ratio.

Debt to income ratio applies to the comparison of an individuals monthly expenses to their monthly income. Lenders use strict debt-to income ratios when qualifying a borrower for a mortgage, so it is imperative that you get a basic understanding of how this is done.

The housing to payment ratio is referred to as your front-end debt-to-income (DTI) ratio and includes all expenses associated with the mortgage – including principal, interest, property taxes and homeowners insurance. To calculate an affordable front-end DTI, multiply 0.3 by your gross (pretax) annual income, then divide by 12.

In contrast, your back-end DTI is the percentage of your gross monthly income that is applied to all other installment debts (i.e., mortgages, student loans, car payments, credit cards, child support etc). One of the first things to do is itemize all of your debts, including credit card bills, personal loans, and car payments.

The back-end DTI shows the lender exactly how much of your earnings go towards your total debt obligations. Generally, they will look for a borrower with a DTI of around 43-55%. If your DTI is below 43% then you have a better chance of qualifying for a loan.

If your DTI is above 43% then you may have a more difficult time meeting the requirements. FHA mortgages allow a higher number with a front-end DTI of 47% of your gross monthly earnings, and a back-end DTI of 57-59%.

How to calculate your debt to income ratio (DTI)

To determine the size of a mortgage you can afford, your total monthly payment, taxes and insurance (PITI) should not exceed 2x to 2.5x your take-home pay or salary after taxes and other withholding are taken into consideration.

The first step is to calculate your gross monthly income.

To do this, simply figure out how much money you are making each month from all of your documentable sources throughout the year and now divide that by 12. If you are married, figure both incomes into the equation.

Remember I said “documentable”.

If you can’t prove it, it didn’t go into your bank account and or you do not claim it on your taxes, then it is not provable income.

Add up all your monthly debts

Things like a car, credit cards, and stuff that will show up on your credit report are what we are looking for. Figure out what percentage of your income is going towards paying off debts. Generally, figures like 5%, 10%, or 20% are used.

Of course, the lower the better, as you will be more likely to be able to keep up with the payments. So, if your income is $4,000 per month and your debts are $500, this would mean that you are currently at an approximate 13% debt to income ratio.

STEP 4: Calculating Your Mortgage Payments

These are some of the major costs a homebuyer faces when buying a home. Once you have all the costs figured out, you’ll want to sit down with your lender or loan officer to locate a realistic mortgage option.

These expenses include, but are not limited to:

Monthly mortgage payment: Principal, interest, taxes, homeowners insurance (PITI) and HOA dues (if applicable).

Homeowners Insurance

Homeowner’s insurance is required to obtain a mortgage. In fact, you’ll be paying for homeowner’s insurance before you even close on the property. Your lender will require that you pay your first year’s insurance premium when you close on your home loan, and it will be included in your monthly mortgage payment.

Homeowners insurance covers the structure of your home and your personal property inside, up to the policy limits. Most policies also cover liability and additional living expenses if something happens to your home.

For example, if a tree falls through your roof or an electrical fire damages half of your house and you can’t stay there for several months while it’s being repaired, homeowners insurance would cover the cost of temporary housing until your home is again habitable.

How much does homeowners insurance cost?

The typical homeowners policy costs between $1,000 to $5,000 per year, depending on where you live. Premiums vary based on factors like location, coverage limits and replacement cost value (RCV) as well as high risk areas for fire or natural disasters.

In general, if you have a $100,000 mortgage on a house that’s worth $550,000 (the value of the house is also called the replacement cost), your lender requires that you have at least $450,000 in liability coverage and $550,000 in coverage for the structure itself. In addition, you’ll want to protect any personal items inside the home with a rider or floater policy.

The more coverage you take out, the higher your premium will be.

Interest Rate

The two main variables that you will have to consider when determining how much you can afford are the loan amount and your interest rate.

Home loans are typically broken up into two types:

Fixed-rate mortgages have an interest rate that is set and does not change for the length of the loan. This provides stability, but if interest rates go down you will miss out on the lower rate. The most common fixed-rate mortgage is a 30-year loan.

Adjustable-rate mortgages (ARMs) start out with a low, fixed rate and then adjust upward or downward after a certain period of time, depending on market conditions at that time. Most ARM loans provide a fixed-rate payment for three to five years and then adjust every year thereafter.

These are also called 3/1 and 5/1 ARMs, which means they start with a fixed-rate and payment for five years, then adjust annually after that.

Private Mortgage Insurance (PMI):

If you do not have a 20% down payment to purchase the home, you will more than likely be subject to paying PMI. If so, this cost will be figured into your monthly mortgage payment.

You pay PMI as part of your monthly mortgage payment until you reach at least 20 percent equity in your home,, but there is no obligation for your lender to do so. This can take quite some time, especially in a rising real estate market where the value of the home increases faster than you can pay down your loan.

PMI can cost between 0.3% to 1% of the original loan amount on an annual basis. That means that if you borrowed $200,000, you may be paying as much as $2,000 a year — or around $167 per month — assuming a PMI rate of 1%.

There are different ways to eliminate mortgage insurance with less than 20% down; you can buy it out as a single premium, which is a lump sum at closing, or through an option called lender paid, which is a less common direction where you would have a higher interest rate that covers the cost of the premium.

Real Estate Taxes:

Real estate taxes are simply the taxes you pay for your home. All residential property requires the homeowner to pay property taxes – prices will vary from city-to-city, state-to-state.

Each town and county sets their own tax rate and the assessor determines the property value. This information is provided to you by your mortgage company, but you may also contact the local tax assessor’s office to confirm or to find out other important information.

Taxes may be paid annually, twice a year or quarterly. Most of the time when you put less than 20% down the lender will require you to include your taxes and insurance with your mortgage payment. In addition to property taxes, some municipalities also charge a municipal tax or supplemental tax – which is usually a fixed amount that doesn’t change year-to-year.

Down payment:

A down payment is required to purchase real estate. The down payment is subtracted from the purchase price of your home. Your mortgage loan will cover the rest of the price of the home.

The minimum amount you’ll need for your down payment depends on the purchase price of the home you’d like to buy and the type of mortgage.

Most conventional loans will require at least 20% down to obtain favorable terms and avoid private mortgage insurance (PMI) however many borrowers choose to only put 3-5% down in today’s market.

Some lenders offer special programs for buyers, however, which may lower the amount needed for a down payment. FHA loans, for example, may allow buyers to qualify with only 3.5% down if they have a credit score of 580 or higher. Down payment assistance programs may be available for buyers in certain areas who meet income qualifications.

In addition to the down payment, you will also need cash reserves on hand to cover closing costs and repairs that come up during the home inspection process.

Closing Costs:

In addition to a down payment, lenders and third parties associated with the transaction will charge fees to close the loan.

These fees may include loan origination fees, credit report fees, attorney fees, appraisal fees, underwriting fees, etc. In general, borrowers can expect to pay approximately 2-4% of the purchase price in closing costs.

While most of these closing costs must be paid by the borrower, some of them can be paid by the seller, split between buyer and seller or even credited by the lender. It is important that you ask your lender what costs are negotiable and which ones are non-negotiable before making an offer on a home.

Points:

Mortgage points are an upfront loan cost that could save money throughout the life of your loan. Mortgage points can be purchased in order to lower the overall interest rate on your loan. A lower interest rate means lower monthly payments as well as less money being paid over the life of the loan.

The cost of a point is 1% of your total loan amount. For example, if you’re borrowing $500,000 to buy a home, each point will cost you $5,000. Usually every 1% paid to buy the interest rate down equates to .25% in rate.

If you are planning on living your home for a long period of time and expect interest rates to rise, it can be a very wise idea to consider that is also typically a tax-deductible expense, of course consult with your accountant or tax professional the impacts to your taxes when you purchase a home.

Bonus Tips

It is always good to undershoot the number you can most afford. It is better to buy a cheaper house and to have extra money, than it is to overdo it and come up short.

Use a mortgage calculator to determine how much you can afford

Lenders tend to use a formula that is very complex to help decide how much a borrower is able to afford. By using a mortgage calculator you will be able to decide for yourself how much you can afford to pay by factoring in your income, debt, and other expenses to see if you qualify for a home loan.

You can start by calculating your gross income on a monthly basis. Then, you can use a mortgage calculator to determine how much house you can afford.

These tools will allow prospective home buyers to get a good estimate as to what their monthly mortgage payments should be.

But be aware that this tool will only be able to give an estimated amount, so it would be wise to speak with a mortgage counselor to get concrete numbers.

Interest rates and guidelines may also vary from lender to lender, so it is always important to first shop around for the best deal before you make your purchase. And in the end, the mortgage lender will have the final say as to how much the monthly payment will be.

If you would like to know exactly how much mortgage you can afford, please call me at 619-379-8999 or email me at [email protected].

If you do not have a 20% down payment to purchase the home, you will more than likely be subject to paying private mortgage insurance (PMI), which will be figured into your monthly mortgage payment.

PMI protects the lender in case you default on your loan and don’t have enough equity built up to sell the home and pay off the loan balance. Private mortgage insurers are for-profit companies that provide this protection for lenders.

Private mortgage insurance (PMI) is an extra mortgage cost that is used to cover the risk to a lender, and that is paid by a borrower in monthly premiums tied into their mortgage payments. It is not for the benefit of the borrower.

This type of insurance is usually required by lenders when a mortgage loan amount is above 80% loan to value (LTV) and the borrower has less than a 20% cash stake in the property. A loan amount above 80% is considered a lot riskier to lenders, and in order to cover this risk, they require insurance that will pay them in case the borrower defaults on the loan.

PMI payments range anywhere from 1% to as high as 1.5% of the loan amount that is amortized yearly and paid monthly throughout the life of their loan as long as the loan amount is above 80%.

For example, let’s say you get a $100,000 loan amount and are required to have mortgage insurance. Your estimated monthly insurance payments would be approximately $100 extra a month. A $200,000 loan amount would equate to approximately $200 a month in extra insurance fees.

As you can see, this money can add up quickly. Also, please keep in mind that this money does not help pay down the mortgage balance, and it is not tax-deductible.

You pay PMI as part of your monthly mortgage payment until you reach at least 20 percent equity in your home.

Because PMI exists for the benefit of the lender rather than the borrower, it would make perfect sense that most borrowers would be curious about either avoiding or canceling their PMI policies in order to save money on their monthly payments.

Although it is possible to eliminate the need to pay for PMI, the money required and process can be difficult for many people.

Here are a few ideas on how to avoid private mortgage insurance (PMI).

1. Make a 20% down payment

The most commonly known way to avoid private mortgage insurance altogether is to make a full 20% down payment when closing on your mortgage.

By putting 20% down, the lender knows you are a serious borrower who is placing a good chunk of money as a down-payment and they only have to extend an 80% loan, which makes it considerably less risky. This is also called an 80% loan to value.

Making anything below a 20% down payment automatically binds a borrower to a PMI plan.

However, having 20% down is easier said than done, and many borrowers are unable to meet this demand. This makes this specific method difficult for a lot of people.

2. Get a Second Mortgage

Another way to avoid the PMI policy would be to take on one of these funny-named loans, also known as “80-10-10” or “80-5-15” mortgages. The secret of this loan lies with the fact that it is actually two instead of one.

Although the thought of two separate loans on one mortgage plan might sound scary, they actually reduce the amount that you have to put down on a home while still avoiding PMI. Someone with just enough cash to make a 10% down payment is going to get a 90% mortgage and be stuck with a PMI premium.

Piggyback loans allow home buyers to take on one mortgage for 80% of the purchase price, and a second for 10% of the purchase price.

Under the program, the two loans make one mortgage at 90% of the purchase price, but act as two separate finance options. That 10% down payment under this program will suffice for the 80%-10%-10% plan, and could end up being even lower at 5% for the 80%-5%-15% plan.

Under this option, the 80% loan will not require PMI, and most lenders who hold this plan won’t require PMI under it due to the smaller lower-risk loans. Like everything else, piggybacks come with their downsides.

For example, the interest rate for the second loan will most likely be higher due to such a short term. While paying it off, you may end up paying a little extra in interest, all to save yourself from PMI.

3. Wait for your equity to rise above 20% loan to value

If you are currently paying mortgage insurance, the only way to cancel the insurance is to have more than 20% equity in your property. Some people will need to build equity over time if the housing markets allow them to eliminate their insurance policies. If your homes increase in value so you have 20% equity, then you can have the insurance canceled.

This will not happen automatically.

You have to call your mortgage servicers and have them review your mortgage and home value to assess if you can have the PMI requirement waived.

Important note:

Please keep in mind that mortgage insurance is not an insurance policy to protect you in case you miss your monthly mortgage payments, but for the lender only. If you fall behind on your monthly payments and you have this type of insurance, you can still lose your home to foreclosure.

It is your lender who would benefit from the insurance because they would still be paid in full even if you stopped making mortgage payments altogether and/or if you were foreclosed on.

To see if you’ll be paying PMI, you can start by talking to your loan officer about the details of your loan. They’ll be able to look at the specifics and let you know the amount you will be paying.

In 2004, Donald Trump told CNN, “I love bad markets!”

In a Trump University audiobook, he had said “I sort of hope” the real estate market crashes.

“How you react to the so-called housing bubble can be a barometer of your business personality. Are you the type of person who takes advantage of positive situations when they present themselves…or do you heed every message of doom and gloom, avoiding risks that could be some remarkable opportunities?” he wrote in a 2005 post on his Trump University blog.

A couple of years later he told the Globe and Mail in March of 2007, “People have been talking about the end of the cycle for 12 years, and I’m excited if it is. “I’ve always made more money in bad markets than in good markets.”

A year before the last market crash of 2008, Trump counseled Trump University students to take advantage of the housing bubble as an investment opportunity. He was “excited” for it to end because of the money he’d make.

“The real estate markets crashed. Now, I don’t want to blame the real estate markets, because I always made a lot of money in bad markets. I love bad markets. You can do very well in a bad market,” he said.

Fast forward to 2020-2021, it looks painfully obvious that there is another commercial property crash that is rearing its ugly head all across the nation and the world.

The economic fallout from the COVID lockdowns forced thousands of companies around the U.S. to have their employees work from home, and many went out of business.

As a result, tens of thousands of commercial buildings sat empty for several months and some for over a year, forcing a severe financial burden on their cash-strapped owners. In addition, these owners had to pay their mortgage with virtually no tenants to help foot the bill, and as it turns out, many have not been able to make their payments for most of the time.

“Even as Covid-19 cases surge world-wide, the arrival of viable vaccines holds the promise of a return to something resembling normality by the middle of next year. But the commercial real-estate sector may never get back to normal, and that could spell trouble for banks. Many banks are concentrated in and dependent on commercial property lending. Banks hold half of all commercial real-estate loans.

The 5,000 or so U.S. community banks, with about a third of total assets, are two to three times as concentrated in commercial real-estate lending as the approximately 30 larger banks. Problems in commercial real estate can hurt banks in two ways. Losses on existing loans can damage earnings directly, and a correction can reduce future lending volumes, impairing an important driver of earnings.

Based on what we know now, things don’t look good.”

Around the same time, a Politico magazine article said, “Commercial real estate is in trouble, and turbulence in the $15 trillion market is threatening to bleed over into the broader financial system just as the U.S. struggles to emerge from a recession.”

Politico reported, “The number of commercial loans that have been packaged into securities going into “special servicing” — where distressed loans are transferred to a new manager hired by bondholders to negotiate a payment plan on their behalf — has steadily increased since March.

“The number of commercial loans that have been packaged into securities going into “special servicing” — where distressed loans are transferred to a new manager hired by bondholders to negotiate a payment plan on their behalf — has steadily increased since March.

And it has become clear that the virus will continue to cut into revenue for some time, so even those property owners who have been able to patch together payments — thanks in part to now-lapsed relief measures passed by Congress — may start to slip.

The loss of paying tenants could touch off a wave of property write-downs and eventual foreclosures on everything from shopping centers to apartment buildings. But it’s not just a pocket of wealthy investors who will get hurt by widespread write-downs. Eighty-seven percent of public pension funds and 73 percent of private pension funds hold real estate investments.

For nearly two years now, many major commercial properties have suffered from low occupancy rates and forced closures due to the Covid-19 pandemic. This is especially true for Hotel properties with $100-200 million dollar mortgages that have remained virtually vacant throughout the crisis.

The facts are that many commercial building owners have not made payments over the last 1-2 years, and their lenders are starting to foreclose upon them for non-payment all across the nation. Investors hold up these loans via commercial mortgage-backed securities that have been bundled and sold on Wall Street all across the globe.

An economic disaster that I predict will become a market crash as soon as investors awake from their slumber and become wise to the media propaganda lying to their ears the whole time.

It has come time for many of them to pay the piper, and it is painfully obvious that many of these property owners barely have two nickels to scratch together. But they won’t tell you that. Quite the contrary.

Now, we will see the actual grave reality for what it is.

A commercial foreclosure crash like the world has never seen.

Major commercial markets like New York and especially Chicago are starting to surge as the foreclosure tsunami rises.

Here are the latest commercial foreclosure casualties. I’m sure Trump is more than ready to use his investing skills to snatch up some great deals in the years to come.

The big question is, “are you ready?”

Below is just a tiny example of the foreclosure fallout. There will undoubtedly be many more that will make this list as the months and years go by.

NEW YORK

Hello Living East Flatbush Apartment Complex

In New York, a judge ruled that Madison Realty Capital can go after the interests of the luxury commercial developer, Eli Karp’s Hello Living East Flatbush apartment complex — and the rest of its portfolio through a UCC foreclosure sale, according to The Real Deal.

Karp founded Hello Living in 2005. He has developed 10 buildings under and six more are allegedly in the pipeline.

Karp said in an interview that Madison “wiped him out” and forced him out of business.

“I can’t get around how this happened,” said Karp. “I have lost everything.”

A spokesperson for Madison said, “We are pleased with the court’s decisive final ruling in favor of Madison. The facts of this case speak for themselves. It is unfortunate that Mr. Karp has a pattern and practice of frivolous litigation against lenders and partners to further his agenda.”

The Kent House

The luxury mixed-use project, Williamsburg residential development Kent House is facing foreclosure auction thios past month for its equity interest in the luxury mixed-use project, at 187 Kent Avenue. The commercial property located at at 187 Kent Avenue has 96 apartments and 31,000 square feet of retail is owned CW Realty.

Invictus Real Estate Partners claimed that CW Realty defaulted on a $10 million mezzanine loan. The entity was created when Invictus Real Estate Partners took over the loan, along with a $78 million senior mortgage, from Prophet Mortgage Opportunity this summer, according to The Real Deal.

Invictus has also pursued foreclosure on the property based on the defaulted $78 million mortgage loan. To counter that, CW Realty on Sept. 17 filed a hardship declaration, a measure under the state’s commercial eviction and foreclosure moratorium to stop certain commercial real property mortgage foreclosure actions from moving forward until Jan. 15, 2022.

CHICAGO

Civic Opera House

The owner of the Civic Opera House commercial property was served with a $195 million foreclosure lawsuit representing the largest case of a downtown Chicago office building in years, according to Crain.

The lender, Wells Fargo’s lawsuit claims the New York investment firm founded by Mark Karasick failed to pay monthly loan payments on the Chicago’s Civic Opera House since May, marking the biggest default for a downtown office building since the pandemic.

601W and Berkley Properties owes $154 million on loans and $28.3 million for late payments on the 915,000-square-foot art deco landmark at 20 North Wacker Drive. The Cook County Circuit Court is expected to appoint real estate services firm Transwestern as the receiver next week.

The Loop

The owner of the Loop 226,000-square-foot office building in Chicago that houses a Morton’s Steakhouse handed the keys back to its lender to avoid foreclosure after failing to sell the property.

The Irish owned REIT, Wilton U.S. Commercial performed a deed in lieu of foreclosure of the 24-story Art Deco building at 65 East Wacker Place to Acres Capital rather than face a foreclosure lawsuit due to missed loan payments, Crain’s reported.

The REIT’s director Iain Finnegan said the building lost some non-profit tenants in the building “due to a lack of state funding” and the pandemic made it too difficult to recover, leaving the company with the choice to either restructure or sell the asset.

Wilton bought the building in 2010 for less than $16 million. The property had been seized by what is now CIBC through a foreclosure. After losing tenants over the years, Wilton struggled to cover the $1.3 million debt service payment in 2019 after generating less than $375,000.

Standard Hotel High Line

The owner of the luxury Standard Hotel High Line, the Hong Kong–based private-equity firm Gaw Capital hasn’t made a mortgage payment since May 2020, according to Crain’s.

The investment firm owes nearly $187 million, according to a foreclosure lawsuit filed recently in U.S. District Court in Manhattan.

Wells Fargo sent the owners a notice of default on their mortgage in June 2020 demanding demanded that Gaw Capital pay back the entire balance, but they failed to make payments for the next 17 months, the lawsuit says.

The loan backing the property is part of commercial mortgage-backed security or CMBS.

According to Curbed, “The 338-room hotel founded by André Balazs was purchased in 2017 by Gaw Capital, a Hong Kong–based private-equity firm led by Goodwin Gaw. Gaw bought the Standard for $340 million, $60 million less than it had been in contract for a few years before, and took out a $170 million acquisition loan from Natixis, a French investment bank that was bullish on hotels at a time when other lenders were pulling back.

“New York’s hospitality sector is a little out of favor at the moment,” Gaw told Forbes at the time. But during the last year and a half, the hospitality sector has fallen more than a little out of favor, with a global pandemic and travel bans making Airbnb and market oversaturation seem like relatively minor woes.

Gaw Capital owns several commercial properties across the country, mainly in San Francisco and the Standard Hotel High Line is its only New York City asset.

If you own shares in Gaw Capital, you may want to pull your money out soon because this news is a big red flag that they are in serious financial trouble.

Over the past year, several Manhattan hotels have permanently closed. The Roosevelt Hotel, which was owned by Pakistan’s national airline company, and the AKA Wall Street hotel, which has since been converted into apartments.

FLORIDA

DoubleTree Hotel by Hilton of Tallahassee

The Tallahassee DoubleTree Hotel by Hilton on Adams Street through his Delaware-based limited liability corporation, IB Tallahassee, LLC., a hotel owned by JT Burnette is going into foreclosure.

A Leon County court ruled on Sept. 24 that unless his company pays more than $32 million owed by the sale date, the property will go up for auction, which was scheduled to be auctioned on Oct. 28, and sold to a sucker buyer for $23 million.

The Westin Cleveland Downtown is facing foreclosure but has found a sucker buyer to possibly buy the property. In later October, the owners through their attorney had asked a judge to approve the sale of the hotel to HEI Hotels & Resorts for $40.2 million, according to a motion and a copy of the agreement the lawyers for receiver Tim Collins filed in Cuyahoga County Common Pleas Court.

The Carew Tower

According to Cincinnati.com, the Carew Tower, one of Downtown’s most iconic buildings, is facing foreclosure and more than $642,000 in delinquent utility bills just over a year after the building was put up for sale.

Lender Veles Partners LLC filed a foreclosure lawsuit against the building’s owner, Greg Power, on Oct. 15 for defaulting on the mortgage, according to Hamilton County Common Pleas Court records.

Veles claims Power owed $9,664,656 in principal on the loan, about $93,630 in interest and $3,594 in late fees as of Oct. 5.

Power — a Downtown-based commercial real estate investor who owns the Carew Tower and the connected 561-room Hilton Cincinnati Netherland Plaza Hotel — was served a summons on Nov. 2.

According to Oregon Live, KKR Real Estate Finance Trust said it plans to take ownership of the 1.2 million square foot mall before the end of the year. The company says payments on its $110 million debt have been overdue since October 2020.

“Upon taking title, which is targeted for the fourth quarter, we’ll begin to plan for a comprehensive redevelopment of the site, which we expect will include multiple uses including residential and creative offices,” said Patrick Mattson, the president and chief operating officer of the company. Bloomberg Law first reported the comments.

KKR loaned $177 million toward a renovation of the Lloyd Center in 2015.

Lloyd Center opened in 1960 as a 100-store, open-air mall, said at the time to be the largest in the world. It was covered in the 1980s with a glass ceiling, then extensively renovated in the 1990s into a more traditional enclosed shopping mall with a central food court.

If you are unable to pay your mortgage, refinance, or get a loan modification, you may be able to qualify for what is called a “deed in lieu of foreclosure.”

A deed in lieu of foreclosure (DIL) is a legal procedure in which you willingly transfer your property’s title (deed) back to the lender.

In return, the lender agrees to release you from all legal obligations to the mortgage contract. This will be done to satisfy a defaulted loan and to prevent foreclosure proceedings.

A DIL is often better than just walking away from your home and letting it fall into foreclosure because it has a less detrimental effect on your credit score.

You can also negotiate with your lender so that they will not legally come after you to collect any money you may owe on the mortgage in back payments and fees after the lender has sold the property.

On the other hand, a deed in lieu is also beneficial for the lender because it avoids the costs and effort required for a foreclosure sale.

What are the elegibility requirements?

You may qualify for a DIL but let me warn you that this is not an easy process. Before your mortgage servicer even considers this option, you must meet specific elegilibility requirements;

You cannot afford your current monthly mortgage payments

The property must be your primary residence, not an abandoned or investment property.

You’re experiencing financial hardship, such as losing your job, reduced income, significant illness, divorce, or another difficulty.

You’re unable to obtain a loan modification and have exhausted all other loan workout options and financial resources available to you.

You tried to sell your property with a licensed real estate brokerage at fair market value for at least 90-120 days but were unsuccessful

You don’t wish to stay in your house due to other circumstances, such as a job relocation

You must have actively explored and exhausted all other options and financial resources available to you.

How do I get a deed in lieu of foreclosure from my lender?

In general, a deed is a right granted by a legal contract based upon mutual agreement; therefore, a deed-in-lieu must be based upon voluntary agreement in good faith.

To proceed with a deed in lieu, both parties must agree to and sign both an Agreement in Lieu of Foreclosure, which outlines the terms of the deed and the deed itself, which transfers legal ownership of the property.

For the agreement to be reached, the property’s appraised market value must be less than the original agreement’s outstanding debt, and the property must not be subject to any 3rd party creditor claims or liens.

A third party escrow service then executes the legal agreement, which will release both you and the lender from the original contract.

Once the agreements are reached and there a clear title, the lender then classifies the original loan as paid and issues a waiver to a deficiency judgment. This will typically go into effect if the property’s sale results in less than what is owed on the debt.

Please be advised that many lenders may not be amenable to a deed in lieu because they believe they will have a better title after a standard foreclosure sale. This is because a trustee’s deed of sale effectively erases any judgment liens and second and third mortgages after a foreclosure. Thus, it would depend on the borrower’s lender whether they will accept a deed in lieu or not.

How will it affect my credit?

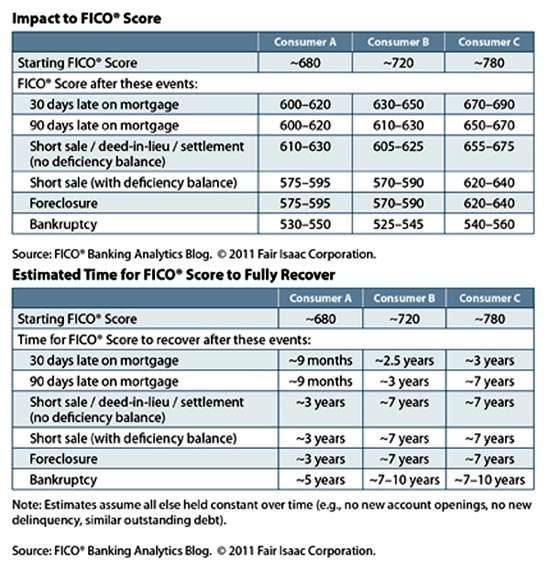

A deed in lieu of foreclosure will cause a negative impact on your credit score. According to a 2011 FICO study, if you begin with a score of approximately 720, it will drop 105 to 125 points off your score; but if you start with a score of 680, you’ll lose 50 to 70 points. But please be aware that your score will drop a lot more if there is any deficiency balance owed.

Here are the charts from FICO;

With that said, you can expect to lose from 50 points minimum to 250 or more points depending on your credit score when you started and if you own a deficiency balance or not. The credit report will also reflect the deed in lieu for seven years, although a borrower can still rebuild their credit.

However, the ill effect on the credit score gradually lessens in time, and you may request its removal from a credit report towards the closing of year seven.

Tax Consequences

Please be aware that if you can complete a deed in lieu of foreclosure, you will still be liable for taxation on the cancellation of indebtedness or COD income. The tax results would be based on whether the loan is classified as a non-recourse loan or a recourse loan.

You can find out if your loan is recourse or non-recourse in your original loan documents that were initially signed by the lender and borrower.

A, if the basic rule of thumb is that if a lender’s only option is to take possession of the property when the borrower defaults, it is a non-recourse loan. However, if the lender can go after the borrower to collect any shortfall when the property is sold, then it is a recourse loan.

A lender will submit a Form 1099-C to the IRS in the case of a shortfall. This is known as the borrower’s COD income.

In the case of a non-recourse loan, the IRS will consider the deed’s tax consequences in lieu as if the borrower had sold the property. If the property’s current market value is less than what is owed, the borrower will have a personal loss, but this is not tax-deductible.

On the other hand, if the property’s value is greater than the outstanding loan, the borrower will have a gain that may not be taxed if he is able to comply with IRS Sec. 121 two-year residency requirement. In the case of a recourse loan, the situation is similar to the non-recourse loan except that the borrower will also be taxed for COD income if the property’s value is less than what is owed. Ordinary income rates will be applied for the COD income.

According to the IRS, the amount of the benefit must be reported as income received under IRC §61(a)(11)3, unless the taxpayer qualifies for an income exclusion under IRC §108.

When can I buy another home?

Most lenders will not offer a loan to a borrower who has filed a deed in lieu for a minimum of two to three years since it will significantly bring down your credit score. The chances of loan approval increase after a few years, especially if a borrower attempts to rebuild their credit score.

But please be aware that some alternative lenders may extend a mortgage to borrowers who maintain good credit score (680 and above) with large down payments in the 25-30% range.

Generally speaking, you will have to wait after a few years as passed and new credit has been established to purchase a home once more.

I first began working on LoanSafe as an online forum to assist people who were having trouble paying their mortgages and at risk of losing their homes to foreclosure due to the home loan crisis that swept across America at that time.

The articles, content, and LoanSafe forum have helped millions of homeowners over the last 13 years either save their homes with a loan modification, obtain a short sale, forbearance, or walk away legally from their underwater mortgages. I have protested at the US Senate house and Wall Street CEO lawns.

My work has been featured in many media publications such as the New York Times, Fox Busines, and Money Magazine, to name a few.

I have even assisted some people with foreclosure defense tactics that I helped pioneer, such as “where my mortgage note?” and the “mortgage audit” to stop paying their loans altogether. From my advice, quite a few of these homeowners lived 5-10 years in their homes without ever making another payment to their lender.

The information contained on LoanSafe is intended to give property owners the best knowledge of the different types of loan workouts, qualifying metrics used by mortgage servicers, and detailing each option’s pros and cons. I also cover the various foreclosure defense strategies that can keep you in your home payment-free that has been used by attorneys and even pro se defendants across the nation, such as filing a lawsuit, bankruptcy, and mortgage auditing.

My extensive loan workout knowledge comes from my mortgage and real estate experience as an ex-loan officer and real estate agent for a decade in Southern California. Since 2007, I have written hundreds of articles on loan modifications and foreclosure defense strategies that have helped millions of American homeowners in the process.

Over the years, I have networked and consulted with various housing advocate agencies like Bruce Marks at NACA and over two dozen law firms nationwide.

Over the years, I have networked and consulted with various housing advocate agencies like Bruce Marks at NACA and over two dozen law firms nationwide.

As we come into the tail end of 2021 and move into 2022, I believe we are quickly moving into another massive foreclosure event that will dwarf the previous one. In fact, I think the recession we are in now due to unemployment will turn into the Great Modern Depression of our era.

As a result of what I forecast ahead, I’m currently in the process of revamping this website and updating it with fresh new content so I can assist people with the most up-to-date information. This website has taken well over a decade to construct, but it is still a work in progress.

I’m self-published, so I do not have a publisher or an editor to go over my content, but if you find any mistakes and or edits, please feel free to email me at [email protected].

Thank you for visiting my website and I hope it helps you!

Please keep in mind that as you consume the content on LoanSafe.org, Moe Bedard is not a lawyer, and the information he presents to you is not intended to be legal advice. If you need an attorney, please consult with a law firm in your state.

This website has Google ads, independent advertisements, paid promotion, and sponsorships to help cover the costs of research, publishing, and hosting. These advertisements do not constitute an endorsement, guarantee, warranty, and or recommendation by LoanSafe.org or Moe Bedard.

22 Mortgage Programs to Buy or Refinance a Home Learn about the various mortgage programs for home buyers and existing homeowners. Quick Links Government Help for Home Buyers Government Mortgage Loans Home Affordable Modification Program (HAMP) Home Affordable...

Learn About LoanSafe and Meet the Team LoanSafe.org is America's #1 mortgage website. Since 2007, we have helped thousands of people for free with their home loans, and we have also saved countless homes in the process. Our great work has been featured in the New...

Refinance Your Mortgage Learn everything you need to know about refinancing your mortgage the right way with LoanSafe. With Mortgage rates currently at all time lows, many believe it is a great time to refinance your mortgage. If you’ve been lucky enough to have had...